To create a statistical model for future returns , in particular the left tail.

Model if often based on historical returns ( the only thing that we can observe)

Future Distribution of Returns(TR) = Function (Historical Returns , Some assumptions)

Modelling assumptions so far

Future Distribution ( WILSHIRE 5000/ index fund) == Historical Distribution ( True for some time but not always)

Currently our distribution of choice is re-scaled T-distribution as it models the data better than normal distribution .

We have also simulated observed distribution from the data

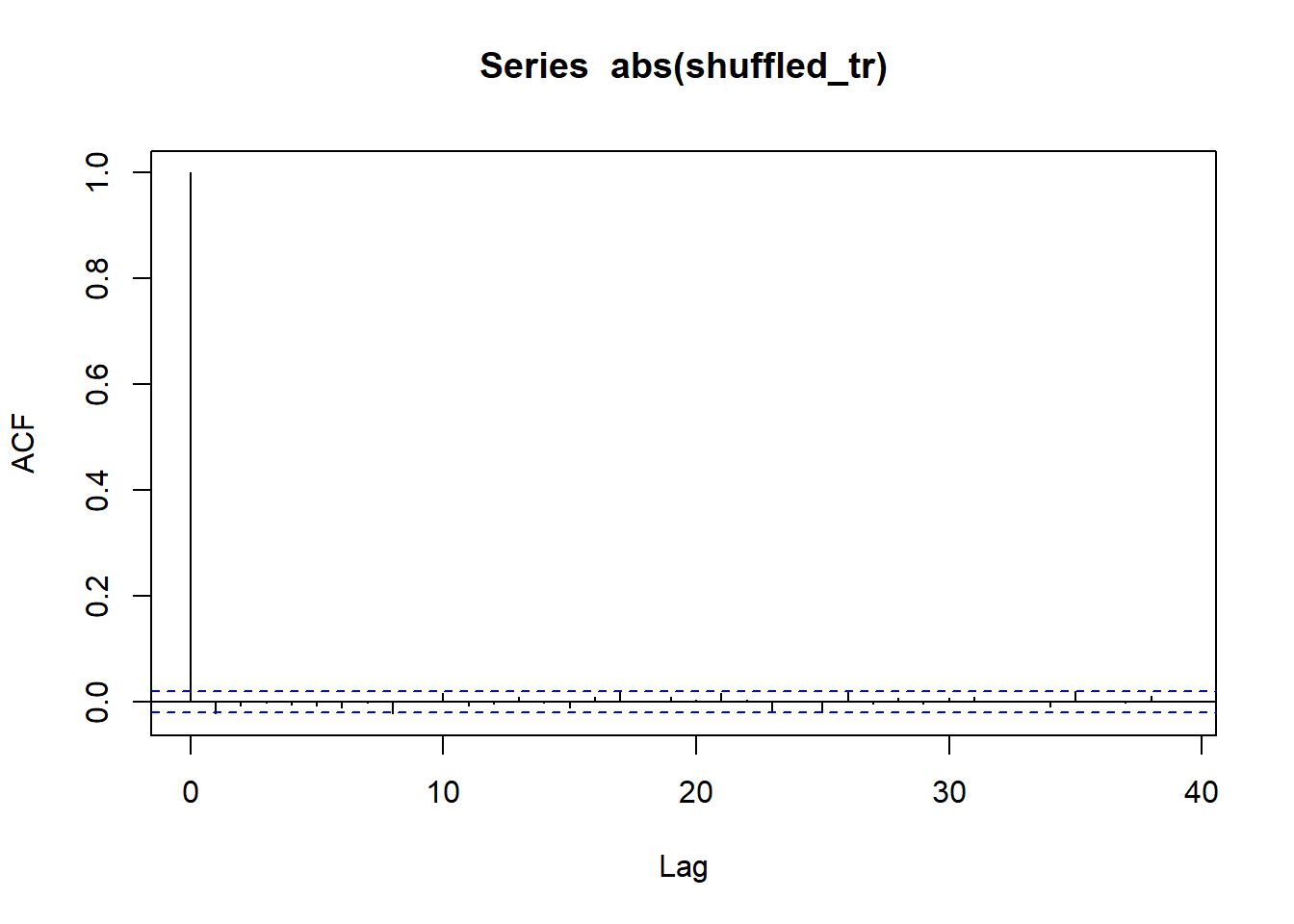

Parameters of historical distribution ( mean, sigma and/ or df) are calculated without paying attention to the ordering of the data

Implies, even if we randomly permeates logret series distribution parameter will still be same.

What if we have some information in the past which can inform us about the future distribution for logret? In other words, what is the impact of serial correlation if any.

Serial correlation

Positive serial correlation - an above average return ( > mean) tend to be followed by another above - average return

Negative serial correlation - above average return is followed by below average return

No correlation / random wal k - an above average return does not increase the likelihood of being followed by an above avg or below avg return.

There was a long history of research in financial markets that look at serial correlation. Now to understand what serial correlation means,

Correlation - let’s start with the correlation between two variables, let’s say, X and Y. The correlation coefficient between X and Y measures how they co-move together. We say that X and Y are positively correlated when they tend to move up and down together. To be more precise, if X is above its mean, then Y is likely to be also above its mean.

Serial correlation - How a variable X and its own past are correlated?

Significance of serial correlation in Finance is associated with the concept of Market Efficiency.

The theory of market efficiency says that the observed price of an asset such as a stock, fully reflects all information about that asset

When new information comes in, it will change the price of the asset. Good news presumably will lead to an increase in its price. Conversely, bad news will lead to a decrease in its price.

Now, because all existing information has been incorporated in the price of an asset, any new information must be a surprise.

If the surprise is good news, the price of the asset will go up, and if the surprise is bad news, the price of the asset will go down. But there is no way to tell ahead of time whether the news is good or bad. So there is no way to tell if the price will go up or down.

This is so called random walk model of prices.

This random walk model just says there is no way to predict if the future price of an asset will go up or go down relative to its current price.

An implication of the random walk model is that returns have no serial correlation. So testing for serial correlation in stock return has been viewed as testing for market efficiency

Motivation & Definition for Volatility Clustering - In financial time series data, it is often observed

Large returns +ve/ -ve negative tend to be followed by more large returns

High Volatility days are followed by more High Volatility days

Low Volatility days are followed by more Low Volatility days

This phenomenon is called Volatility clustering

It is calculated mathematically by measuring autocorrelation of absolute values of log returns

A time series exhibiting Volatility clustering implies ordering of the data is important

Strong volatility clustering implies we can predict volatility of stock prices for future values based on the past values.

This is exploited in GARCH model ( Generalized Auto-regressive Conditional Heteroskedasticity)

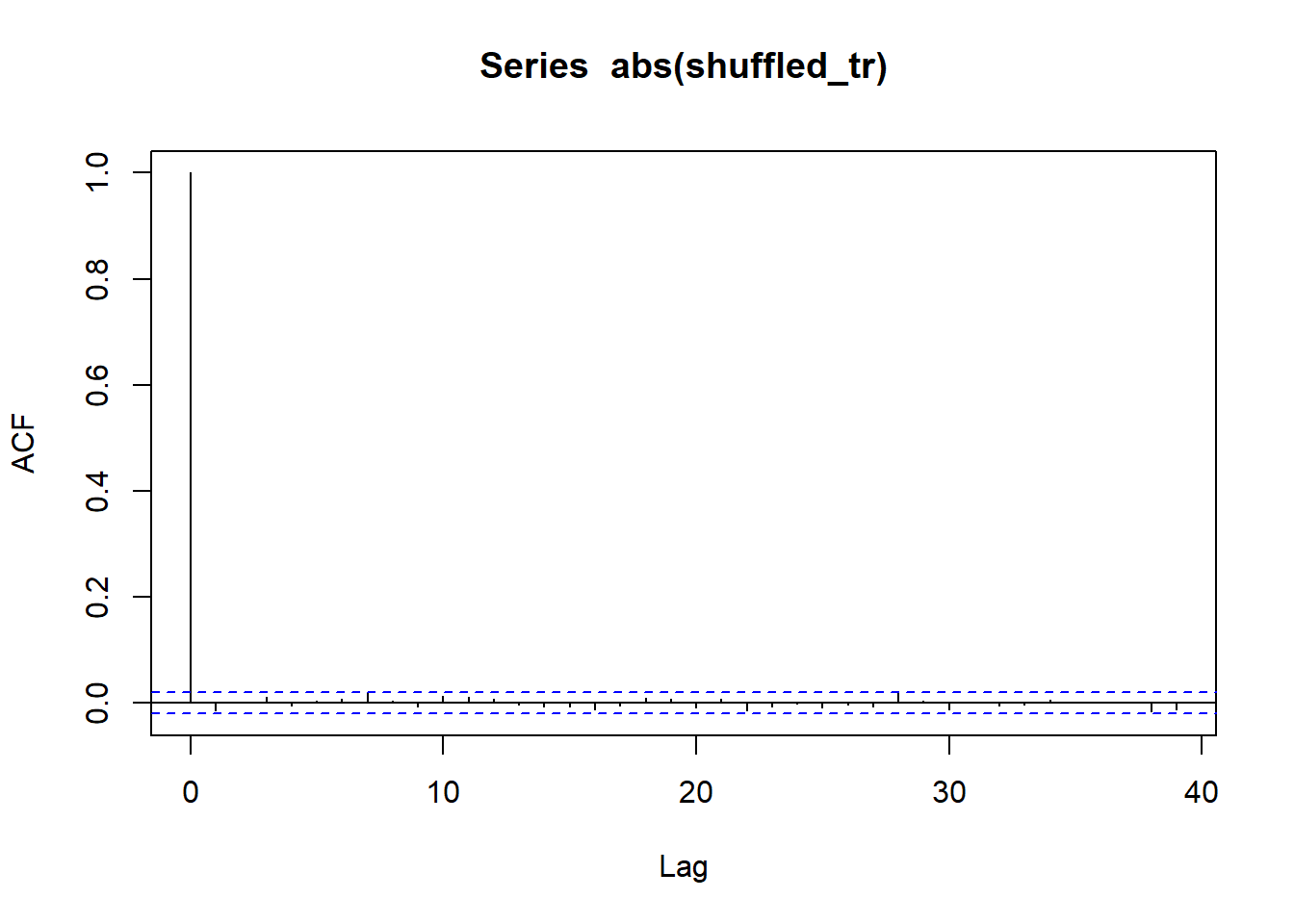

We can test volatility clustering/ effect of ordering by

Plotting acf on absolute values of logreturns - ( Should show strong evidence of serial correlation )

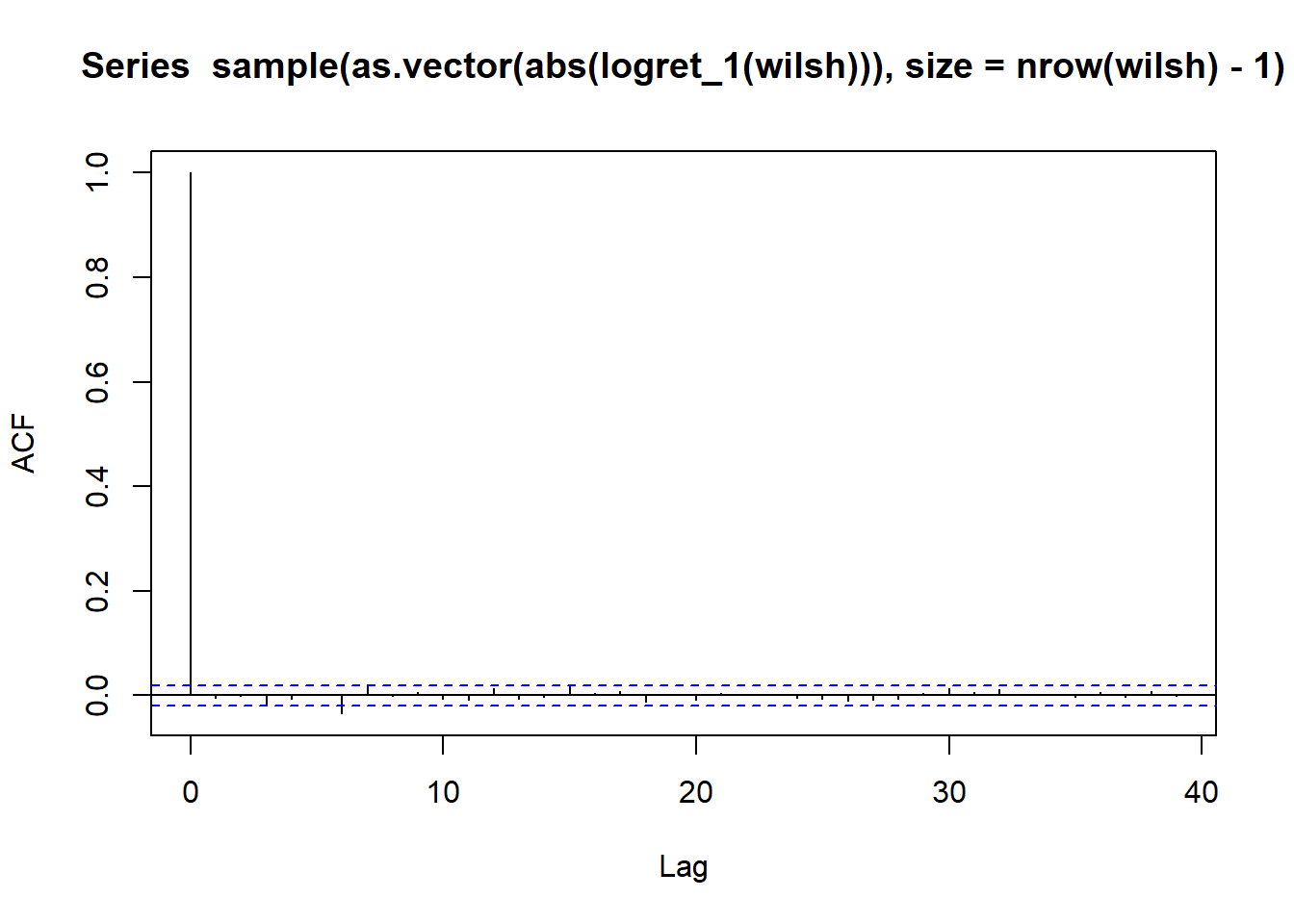

Shuffling/ Permeating returns and apply same logic again ( Should show no evidence of serial correlation on shuffled series)

GARCH model

WILSHIRE 5000 ACF plot indicates no/ weak evidence of serial correlation => Difficult to predict mean of future values based on historical values

WILSHIRE 5000 ABS(ACF) plot indicates strong volatility clustering =>Volatility / Standard Deviation is changing over time in a predictable manner.

What we want is a statistical model which allows us to predict future volatility- GARCH

GARCH model has many extensions. We are going to focus on GARCH(1,1). It is one of the simplest GARCH model .But it does a very good job on WILSHIRE 5000 data in modelling volatility clustering.

GARCH(1,1)-normal model is equivalent to normal model when we assume constant variance.

Equations

Notations:

: Expected Returns

: Unexpected Returns

: Total returns of series with time varying volatility

: predictable variance of changing over time

: Normal Distribution

If is constant above equation reduces to normal model for logret.

For Volatility clustering to happen:

GARCH(1,1)-t model is equivalent to normal model when we assume constant variance.

Equations

Here we replace chosen distribution (norm) with re-scaled -t model

1-day ahead garch model can be simulated using ugarchboot function.

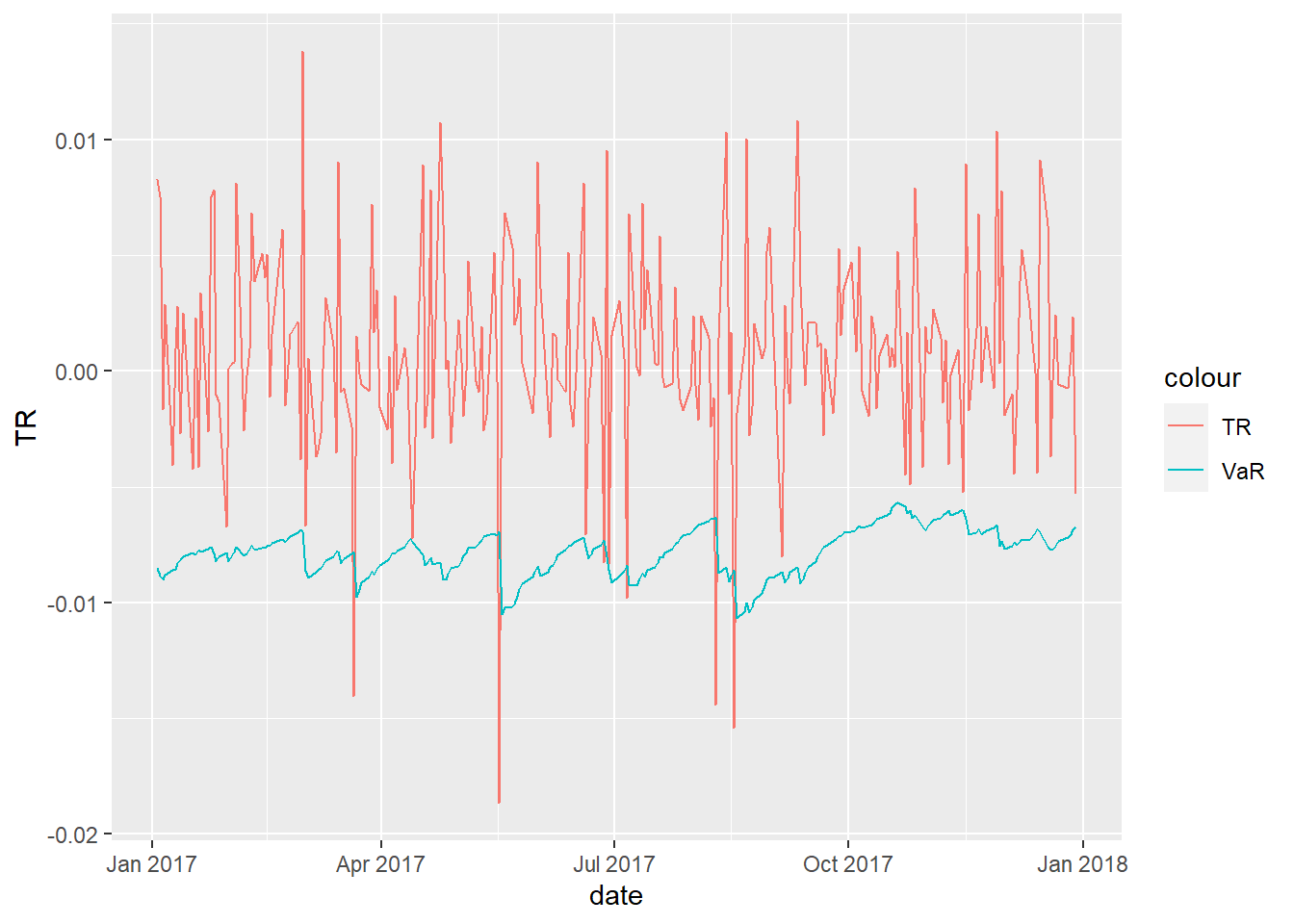

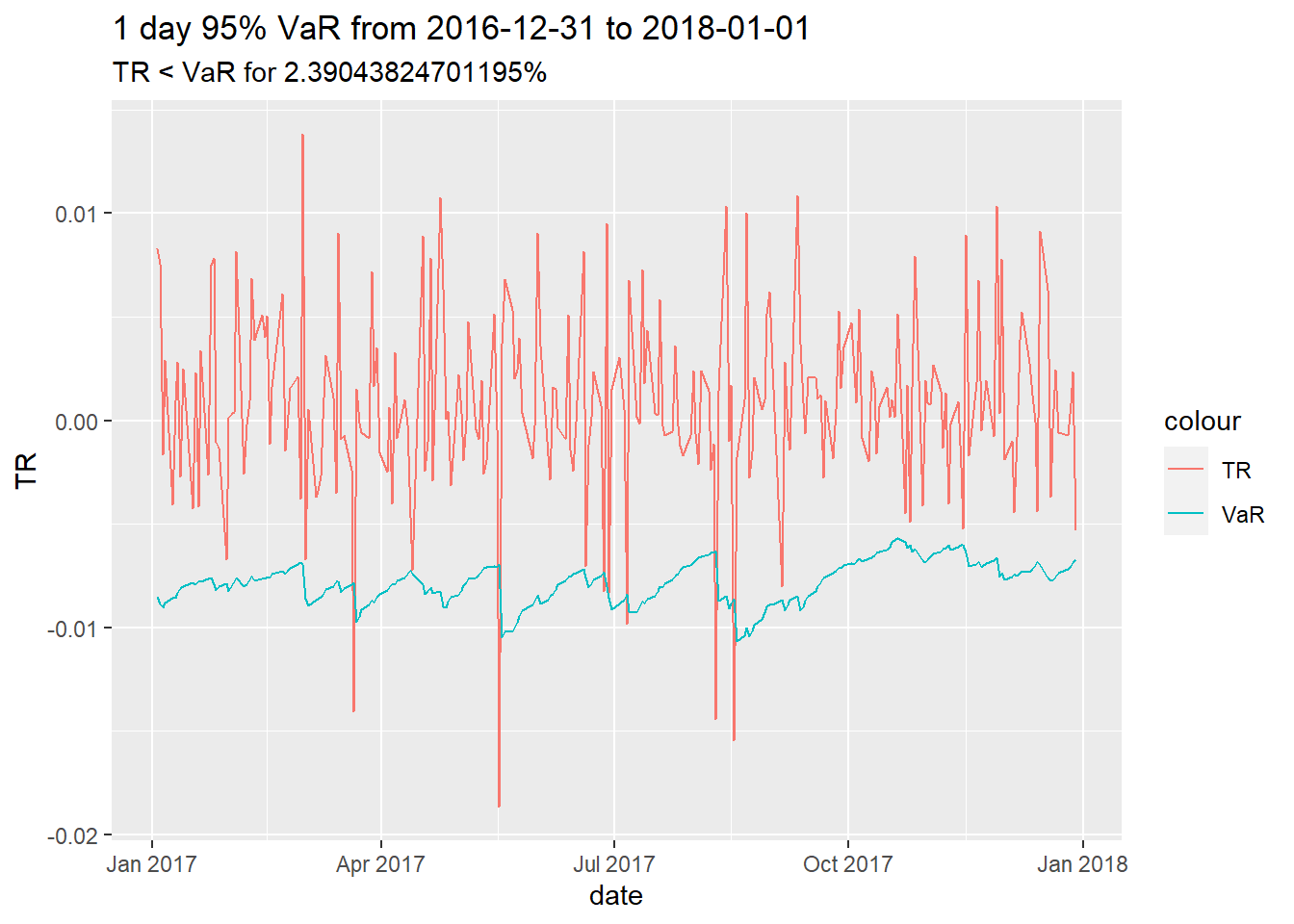

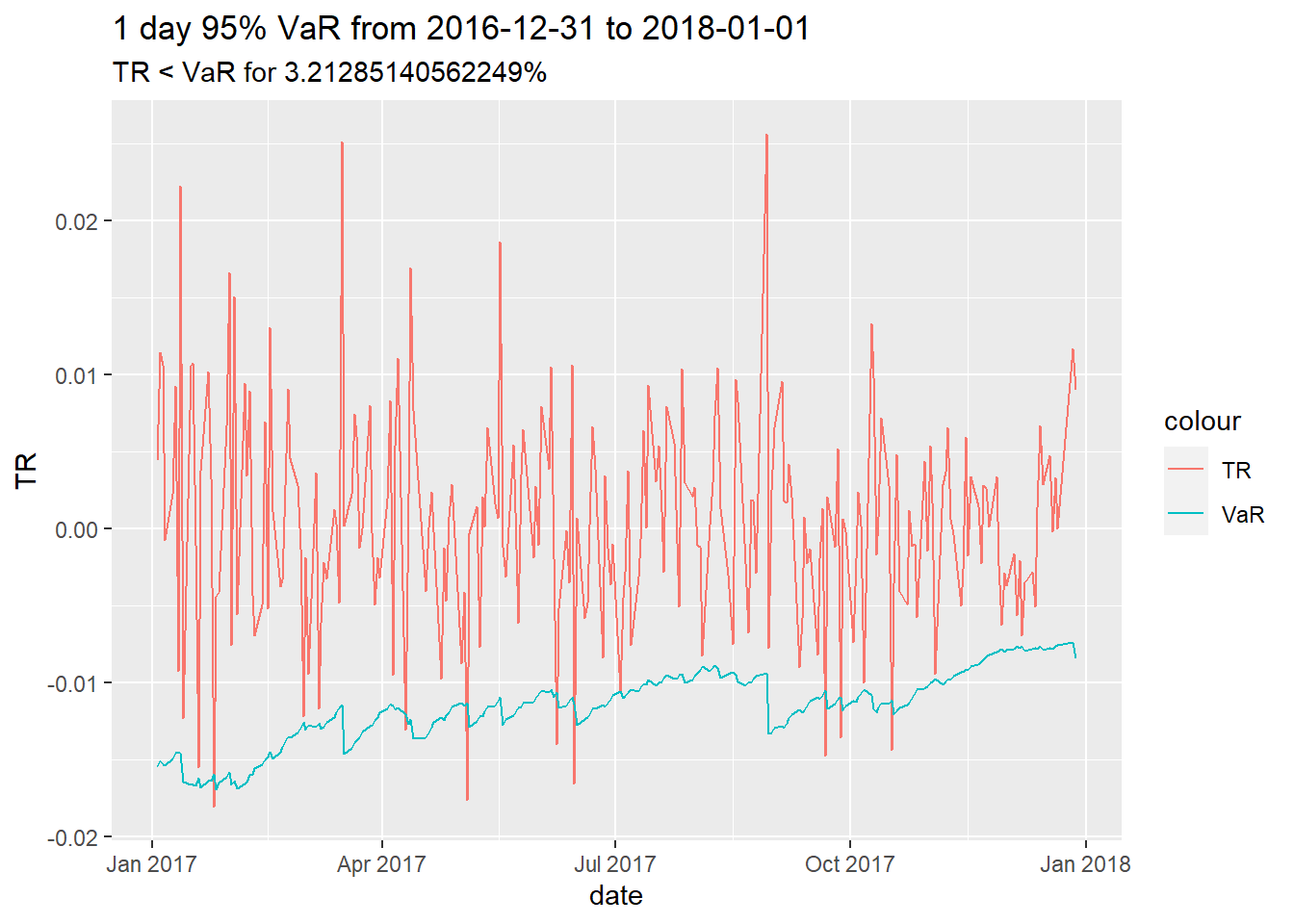

VaR and ES from garch take time ordering into account

When Fitted values are low => VaR and ES are also low.( Only apply for 1-day)

Why is GARCH model better?

When volatility is high => Risk is also high => Portfolio manager can take some action to mitigate risk

When volatility is low => Risk is low => No action as risk reduction may be costlier to portfolio.

VaR graph can be produced by using ugarchroll function.

Summary

Basics of Financial risk management

Analyze logret of portfolio

Distribution: typically non-normal

We also have volatility clustering : a behavior typical of asset returns

GARCH(1,1)-t can explain both

VaR and ES change over time

Ideas can be applied to different types of portfolios

Margin borrowing: $10 K stocks with

$5K your money

$5k from a brokerage firm

This is a margin position

You are hoping to make money from stock price going up

Risk -> Price can go down. How much money can you afford to loose -> ES over a time period( like 10 days) with a certain confidence level( like 95%)

Stock/Bond Portfolio:

Retirement Account

50% US Equities

50% long term corporate bond

Plan to retire in 1 year

No plan to add more money or take money out next year

How much can you loose in 1 year?

Can you afford to loose this amount of money for retirement in 1 year?

Imports

library(quantmod)

Loading required package: xts

Loading required package: zoo

Attaching package: 'zoo'

The following objects are masked from 'package:base':

as.Date, as.Date.numeric

Loading required package: TTR

Registered S3 method overwritten by 'quantmod':

method from

as.zoo.data.frame zoo

The following objects are masked from 'package:base':

cbind, rbind

library(rugarch)

Loading required package: parallel

Attaching package: 'rugarch'

The following object is masked from 'package:purrr':

reduce

The following object is masked from 'package:stats':

sigma

Set Seed.

RNGkind(sample.kind="Rounding") set.seed(123789)

Functions

Show the code

filterSeries <-function(s, date_filter="1979-12-31/2017-12-31", new_name='TR'){ s <-na.omit(s); s s <- s[date_filter]; snames(s) <- new_name; sreturn(s)}getSeries <-function(name, date_filter="1979-12-31/2017-12-31", src='FRED', new_name='TR', auto.assign=FALSE){ s <-getSymbols(name, src=src, auto.assign = auto.assign); s s <-filterSeries(s)return(s)}get_df <-function(tbl){ df <-data.frame(date=index(tbl), TR=as.numeric(tbl$TR))return(df)}logret_1 <-function(tbl){return(diff(log(tbl))[-1])}aggr_fn <-function(tbl, fn){ result <-fn(tbl, sum)return(result)}logret_w <-partial(aggr_fn, fn = apply.weekly)logret_m <-partial(aggr_fn, fn = apply.monthly)logret_q <-partial(aggr_fn, fn = apply.quarterly)logret_a <-partial(aggr_fn, fn = apply.yearly)logret_ndays <-function(tbl, days=10){ len_tbl <- (nrow(tbl)-days+1) new_TR <-sapply(seq(1:len_tbl), function(i){sum(tbl[i:(i+days-1)]) }) tbl[1:len_tbl]$TR <- new_TRreturn(tbl[1:len_tbl])}ret <-function(logret){return(exp(logret)-1)}get_norm_series <-function(mu, sig, n=100000, set_seed=TRUE){if (set_seed){RNGkind(sample.kind="Rounding")set.seed(123789) }return(rnorm(n,mu, sig)) }get_sim_series <-function(s, n=100000, set_seed=TRUE){if (set_seed){RNGkind(sample.kind="Rounding")set.seed(123789) }return(sample(as.vector(s), n, replace=TRUE))}get_t_series <-function(mu, sig, df, n=100000, set_seed=TRUE){if (set_seed){RNGkind(sample.kind="Rounding")set.seed(123789) }return(rt.scaled(n,mean=mu,sd=sig,df=df)) }get_norm_series_from_s <-function(s, n=100000, set_seed=TRUE){ mu =mean(s) sig =sd(s)return(get_norm_series(mu, sig, n=n, set_seed = set_seed))}get_fit_params <-function(s){ fitpars <- s |>as.vector() |>fitdistr(densfun='t') return(fitpars)}get_t_series_from_s <-function(s, n=100000, fitpars=NULL, set_seed=TRUE){if(is.null(fitpars)){ fitpars <- s |>get_fit_params() } t.fit <- fitparsreturn(get_t_series(mu=t.fit$estimate[1], sig=t.fit$estimate[2], df=t.fit$estimate[3], n=n, set_seed=set_seed))}get_sim_VaR <-function(s, alpha=0.05){return(quantile(s, alpha) |>unname())}get_sim_ES <-function(s, VaR){# VaR <- get_sim_VaR(s, alpha=alpha)return(mean(s[s<VaR]))}get_VaR <-function(tbl,alpha=0.05){ mu =mean(tbl) sig =sd(tbl) VaR =qnorm(alpha, mean=mu, sd=sig) #quantile of normal distribution(only not for any other distribution)return(VaR)}get_ES <-function(tbl, alpha=0.05){ mu =mean(tbl) sig =sd(tbl) ES = mu - sig*dnorm(qnorm(alpha, mean=0, sd=1), 0, 1)/alpha #quantile of normal distribution(only not for any other distribution)return(ES)}expected_loss <-function(portfolio, risk_num){ #95% confidence that we won't loose more than this amountreturn(portfolio*(exp(risk_num)-1))}err <-function(a, b){return((a-b)/a*100)}get_dist_plot <-function(tbl){ mu =mean(tbl) sig =sd(tbl) p <-get_df(tbl) |>ggplot(mapping =aes(x=TR)) +geom_histogram(aes(y=after_stat(density)), colour="black", fill="white", bins=100)+geom_density(alpha=.2, fill="violet") +geom_vline(aes(xintercept=mu),color="brown", linetype="dashed", linewidth=1) +geom_vline(aes(xintercept=mu+2*sig),color="brown", linetype="dashed", linewidth=0.1) +geom_vline(aes(xintercept=mu-2*sig),color="brown", linetype="dashed", linewidth=0.1) +labs(title=glue("Distribution of TR: mu={round(mu, 8)}, sigma={round(sig, 8)}"), y='count')return(p)}get_VaR_plot <-function(tbl, alpha=0.05){ mu =mean(tbl) sig =sd(tbl) VaR =qnorm(alpha, mean=mu, sd=sig) p <-get_df(tbl) |>ggplot(mapping =aes(x=TR)) +geom_histogram(aes(y=after_stat(density)), colour="black", fill="white", bins=100)+geom_density(alpha=.2, fill="violet") +geom_vline(aes(xintercept=mu),color="brown", linetype="dashed", linewidth=1) +geom_vline(aes(xintercept=VaR),color="brown", linewidth=1) +labs(title=glue("Distribution of TR: mu: {round(mu, 8)}, sigma: {round(sig, 6)}, VaR({alpha}): {round(VaR, 6)}"), y='count')return(p)}get_comp_plot <-function(s, alpha=0.05){ mu <-mean(s) sig <-sd(s) norm_s <-get_norm_series(mu, sig) VaR <- norm_s |>get_sim_VaR(); VaR ES <- norm_s |>get_sim_ES(VaR=VaR); ES s_sim <- s |>get_sim_series() VaR_sim <- s_sim|>get_sim_VaR(); VaR_sim ES_sim <- s_sim |>get_sim_ES(VaR=VaR_sim); ES_sim err_VaR <-err(VaR, VaR_sim) |>round(digits =2) err_ES <-err(ES, ES_sim) |>round(digits =2) p <-data.frame(TR=s_sim, TR2=norm_s) |>ggplot() +geom_density(mapping =aes(x=TR), alpha=.2, fill="violet") +geom_density(mapping =aes(x=TR2), alpha=.2, fill="white") +geom_vline(aes(xintercept=ES_sim),color="brown", linetype="dashed", linewidth=1) +geom_vline(aes(xintercept=ES),color="blue", linetype="dashed", linewidth=1) +geom_vline(aes(xintercept=VaR_sim),color="brown", linewidth=1) +geom_vline(aes(xintercept=VaR),color="blue", linewidth=1) +labs(title=glue("Distribution of TR alpha({alpha}): \n VaR_norm(blue): {round(VaR, 6)},VaR_sim(brown): {round(VaR_sim, 6)}, Error: {round(err(VaR, VaR_sim), 2)}% \n ES_norm: {round(ES, 6)},ES_sim: {round(ES_sim, 6)}, Error: {round(err(ES, ES_sim), 2)}%"), y='count')return(p)}do_analysis <-function(s, alpha=0.05){ modelname1 <-"Norm" VaR1 <- s |>get_VaR() |>as.double() ES1 <- s |>get_ES() |>as.double()# df[nrow(df) + 1,] <- c(modelname, VaR, ES) modelname2 <-"NormSim" norm_series <- s |>get_norm_series_from_s() VaR2 <- norm_series|>get_sim_VaR(alpha=alpha) |>as.double() ES2 <- norm_series |>get_sim_ES(VaR=VaR2) |>as.double()# df[nrow(df) + 1,] <- c(modelname, VaR, ES) modelname3 <-"T-Sim" t_series <- s |>get_t_series_from_s() VaR3 <- t_series|>get_sim_VaR(alpha=alpha) |>as.double() ES3 <- t_series |>get_sim_ES(VaR=VaR3) |>as.double()# df[nrow(df) + 1,] <- c(modelname, VaR, ES) modelname4 <-"Sim" sim_series <- s |>get_sim_series() VaR4 <- sim_series|>get_sim_VaR(alpha=alpha) |>as.double() ES4 <- sim_series |>get_sim_ES(VaR=VaR4) |>as.double() model_names <-c(modelname1, modelname2, modelname3, modelname4) VaRs <-c(VaR1, VaR2, VaR3, VaR4) ESs <-c(ES1, ES2, ES3, ES4)return(data.frame(ModelName=model_names, VaR=VaRs, ES=ESs))}get_multi_day_series <-function(s, days=10, sampling_func=get_sim_series, n=100000, set_seed=TRUE){if (set_seed){RNGkind(sample.kind="Rounding")set.seed(123789) } rvec <-rep(0, n)for( i in1:days){ rvec <- rvec +sampling_func(s=s, n=n, set_seed=FALSE)# print(rvec |> head()) }return(rvec)}get_multi_day_series_block <-function(s,days=10, n=100000, set_seed=TRUE){if (set_seed){RNGkind(sample.kind="Rounding")set.seed(123789) } rdat <- s |>as.vector() rvec <-rep(0, n) posn <-seq(from=1, to=(length(rdat)-days+1), by=1) rpos <-sample(posn, size=n, replace=TRUE)for( i in1:days){ rvec <- rvec + rdat[rpos] rpos <- rpos+1 }return(rvec)}do_multi_analysis <-function(rvec, days=10, alpha=0.05){ modelname1 <-glue("student-t({days})") fitspars <- rvec |>get_fit_params() #; fitspars sampling_func_tdist <-partial(get_t_series_from_s, fitpars = fitspars) s1 <- rvec |>get_multi_day_series(sampling_func=sampling_func_tdist) VaR1 <- s1 |>get_sim_VaR(alpha=alpha) |>as.double() ES1 <- s1 |>get_sim_ES(VaR=VaR1) |>as.double() modelname2 <-glue("IID({days})") s2 <- rvec |>get_multi_day_series(days=days) VaR2 <- s2 |>get_sim_VaR(alpha=alpha) |>as.double() ES2 <- s2 |>get_sim_ES(VaR=VaR2) |>as.double() modelname3 <-glue("consecutive({days})") s3 <- rvec |>logret_ndays(days=days) |>get_sim_series(set_seed =TRUE) VaR3 <- s3 |>get_sim_VaR(alpha=alpha) |>as.double() ES3 <- s3 |>get_sim_ES(VaR=VaR3) |>as.double() model_names <-c(modelname1, modelname2, modelname3) VaRs <-c(VaR1, VaR2, VaR3) ESs <-c(ES1, ES2, ES3)return(data.frame(ModelName=model_names, VaR=VaRs, ES=ESs))}expected_loss_df <-function(df, portfolio=1000){ expected_loss_port =partial(expected_loss, portfolio=portfolio) df$VaR <-sapply(df$VaR, expected_loss_port) df$ES <-sapply(df$ES, expected_loss_port)return(df)}

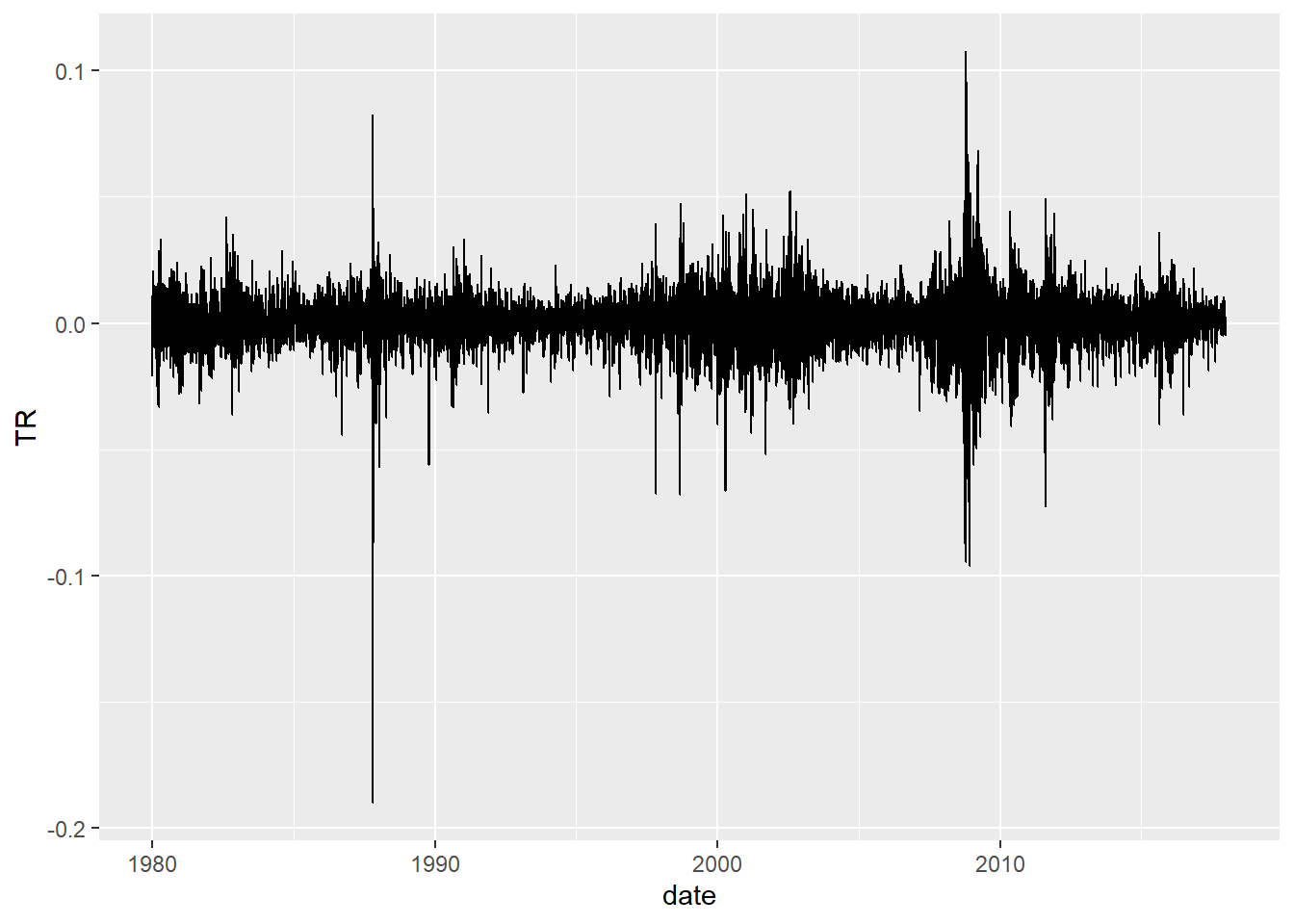

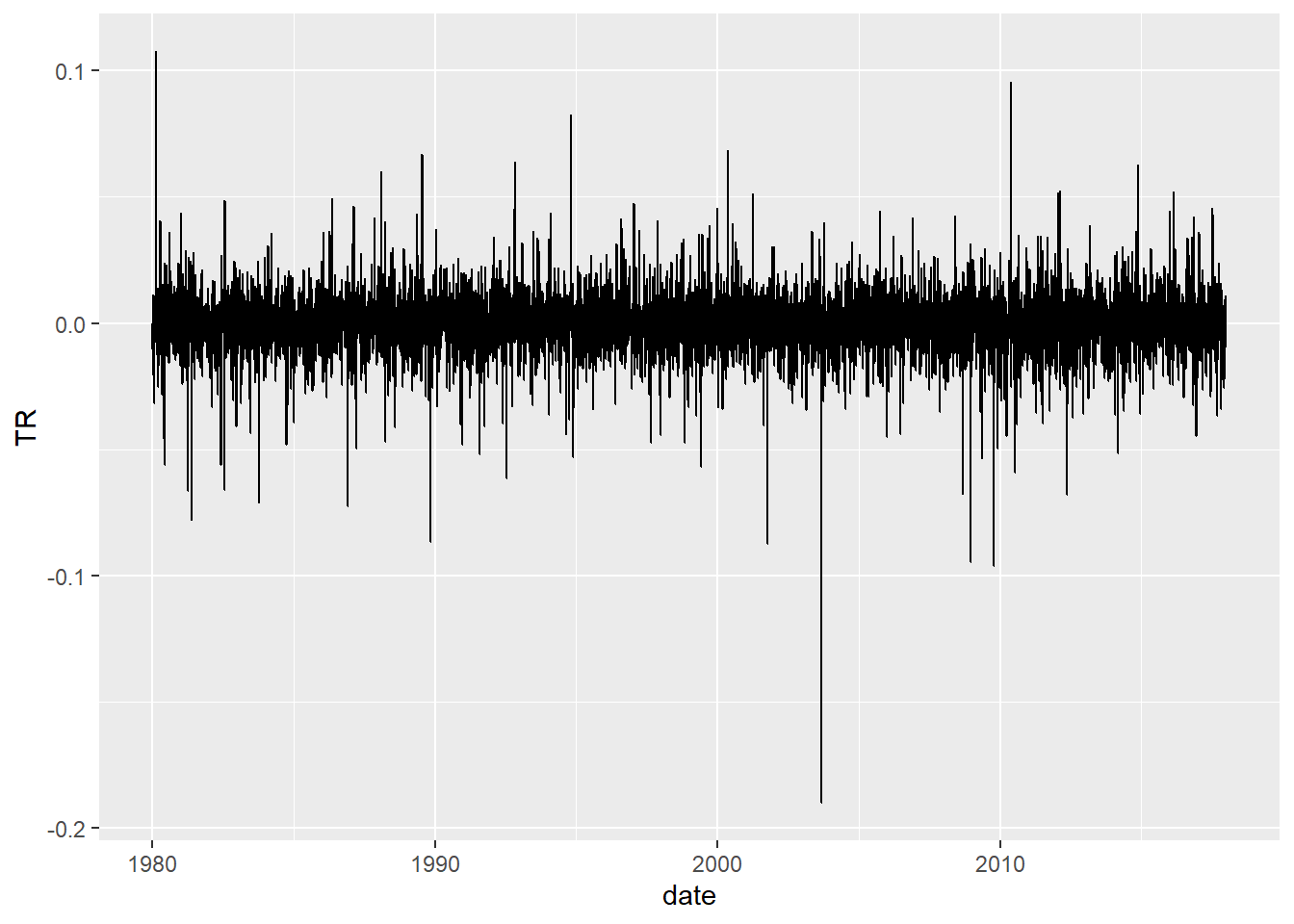

Future Vs Historical Distribution

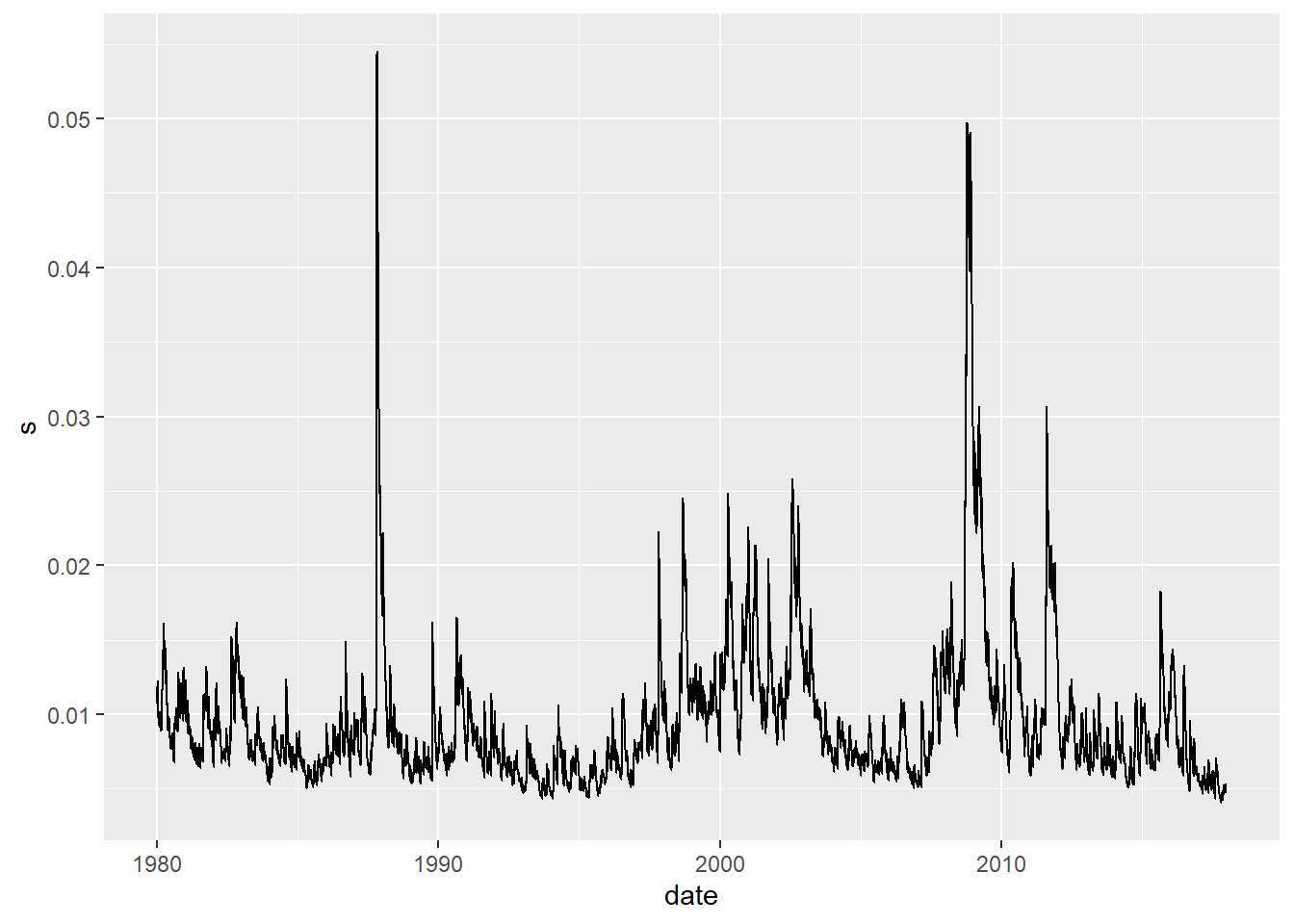

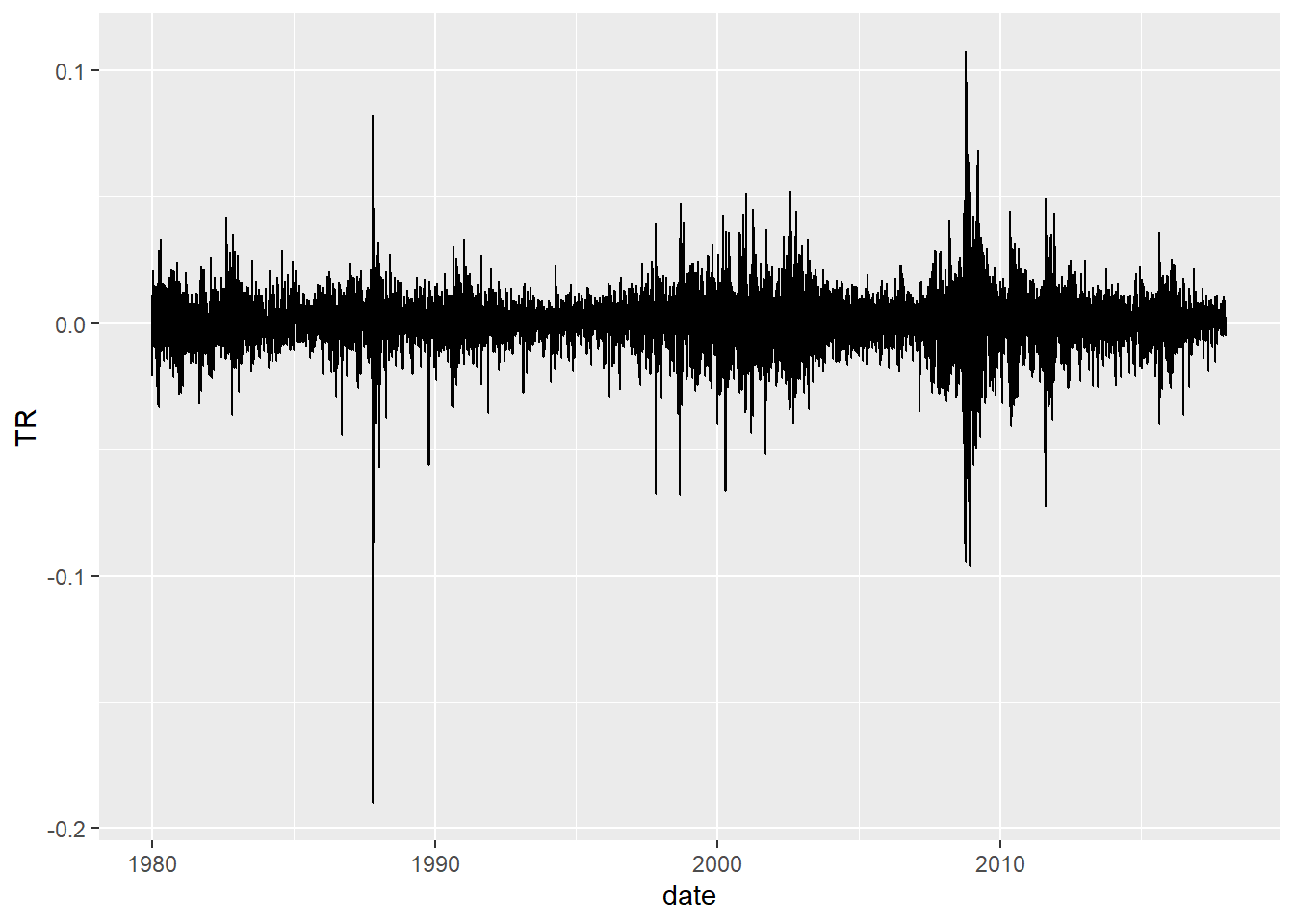

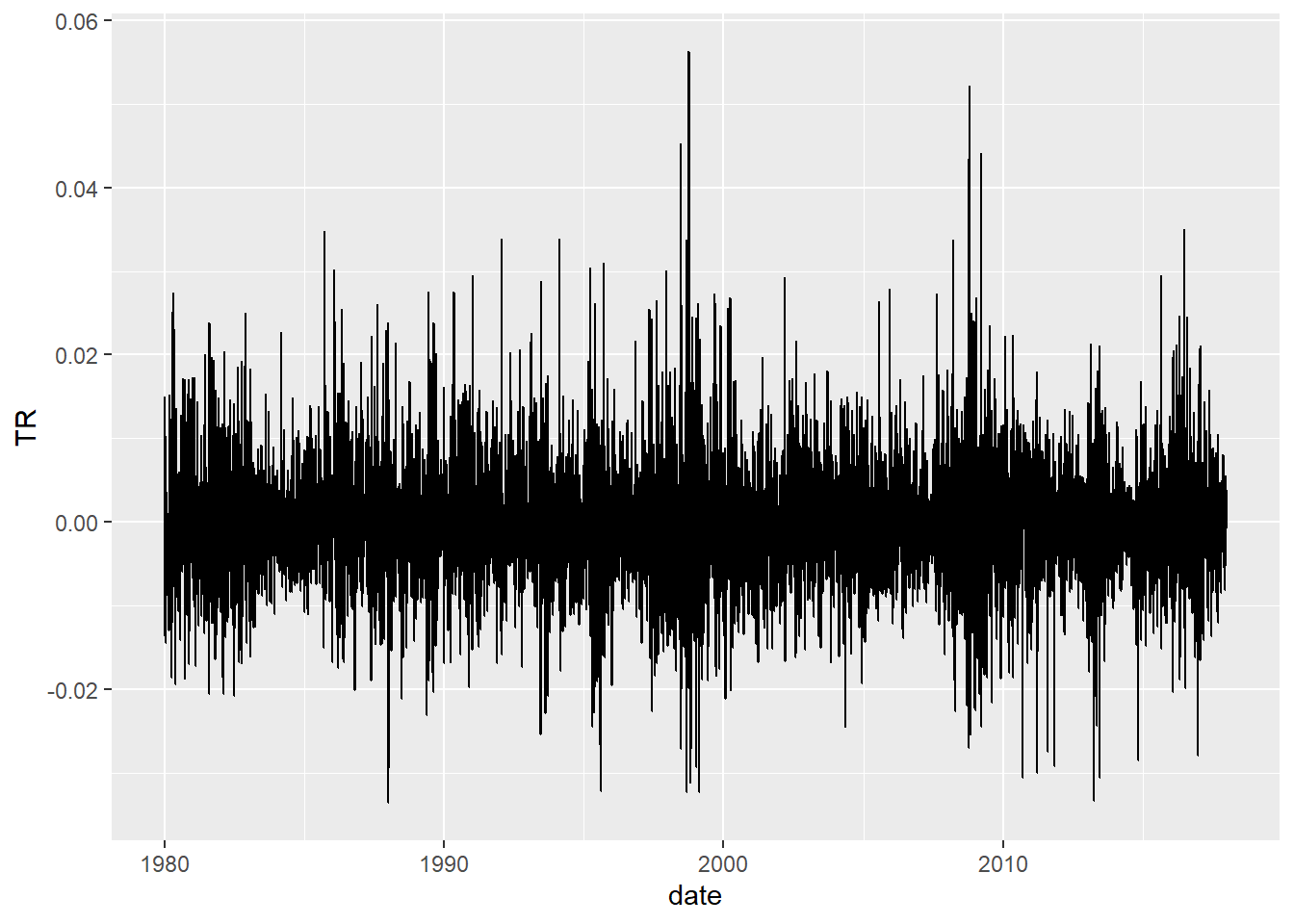

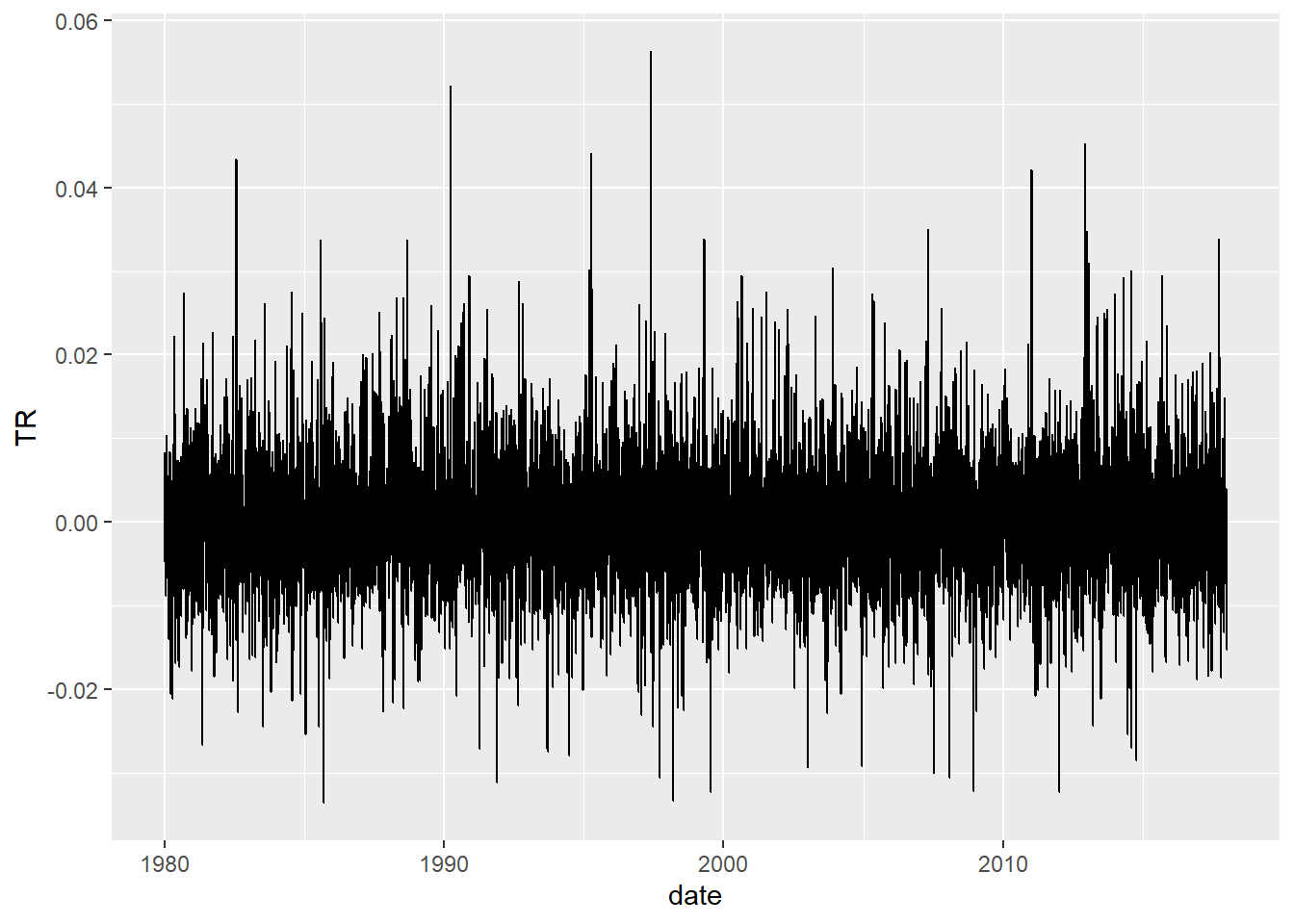

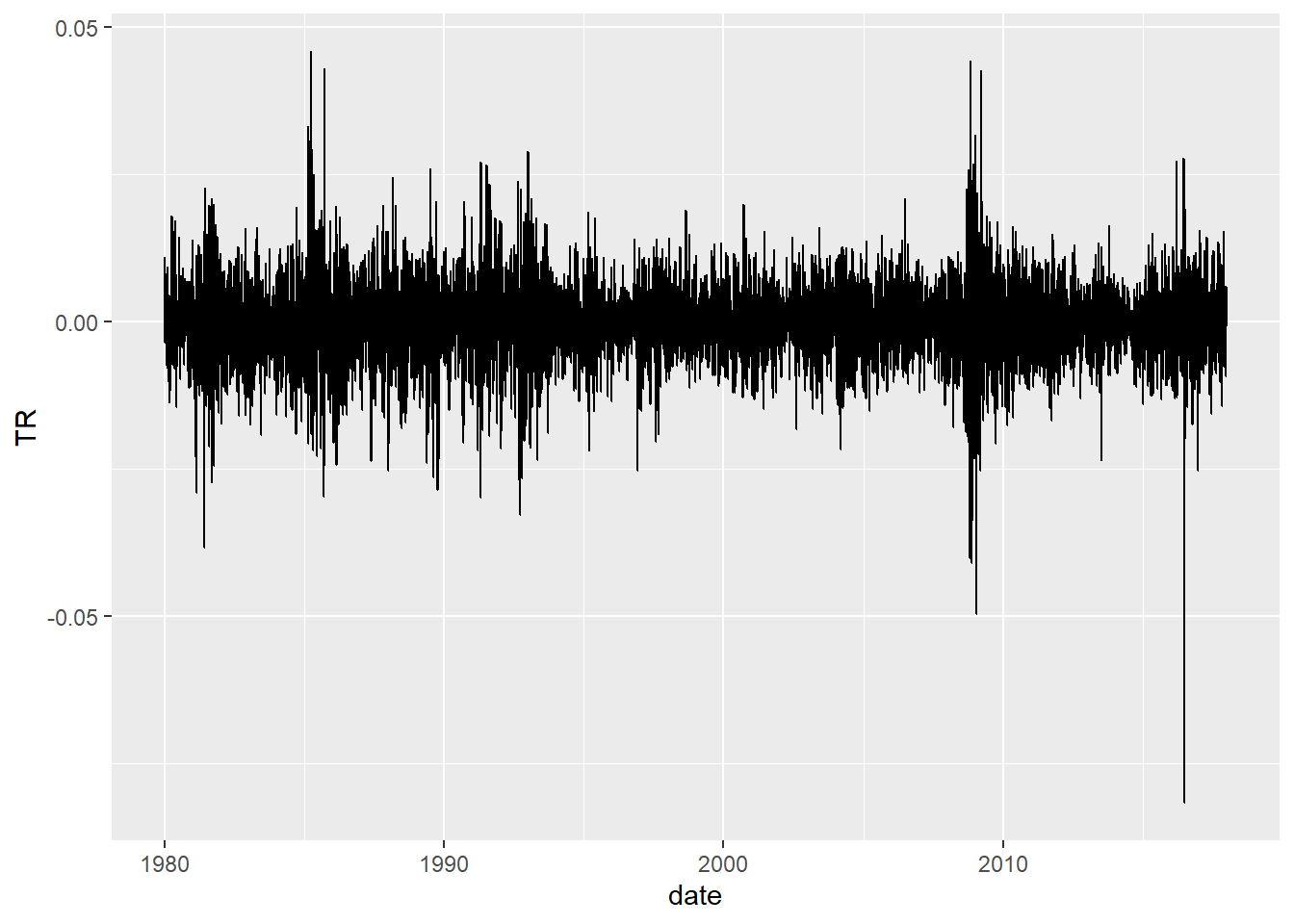

wilsh <-getSeries("WILL5000IND")wilsh |>head(2)

TR

1979-12-31 1.90

1980-01-02 1.86

wilsh |>tail(2)

TR

2017-12-28 124.33

2017-12-29 123.67

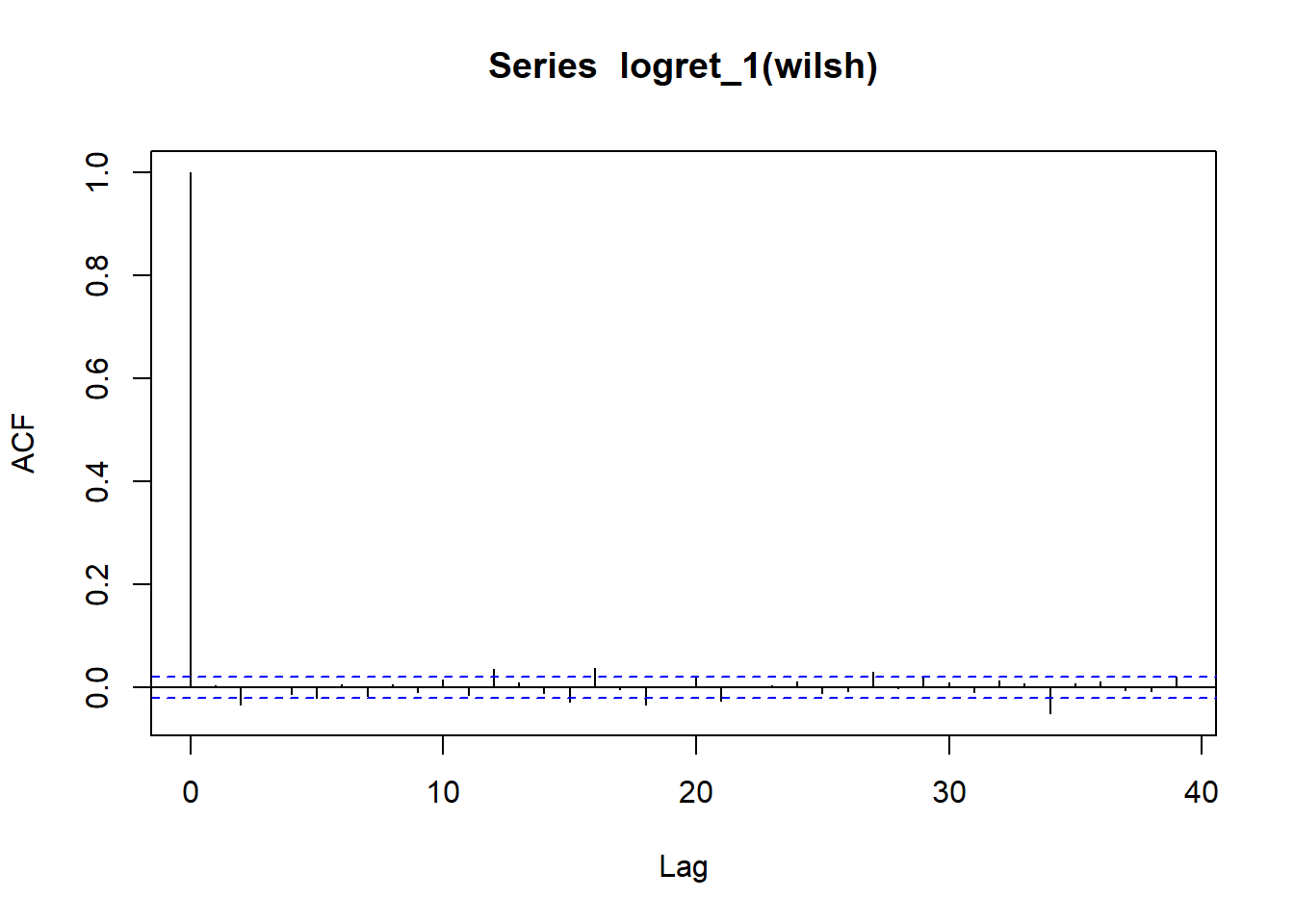

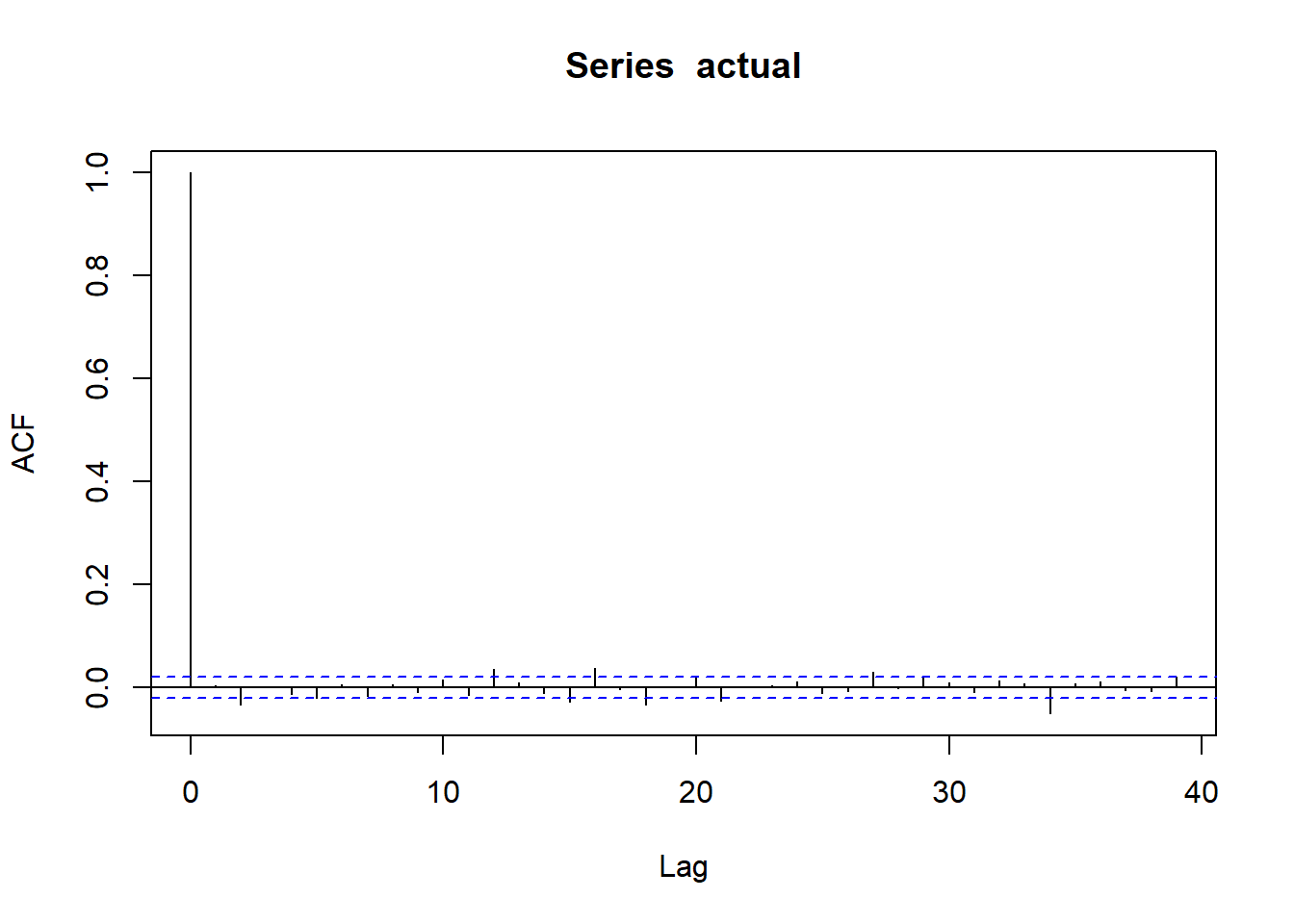

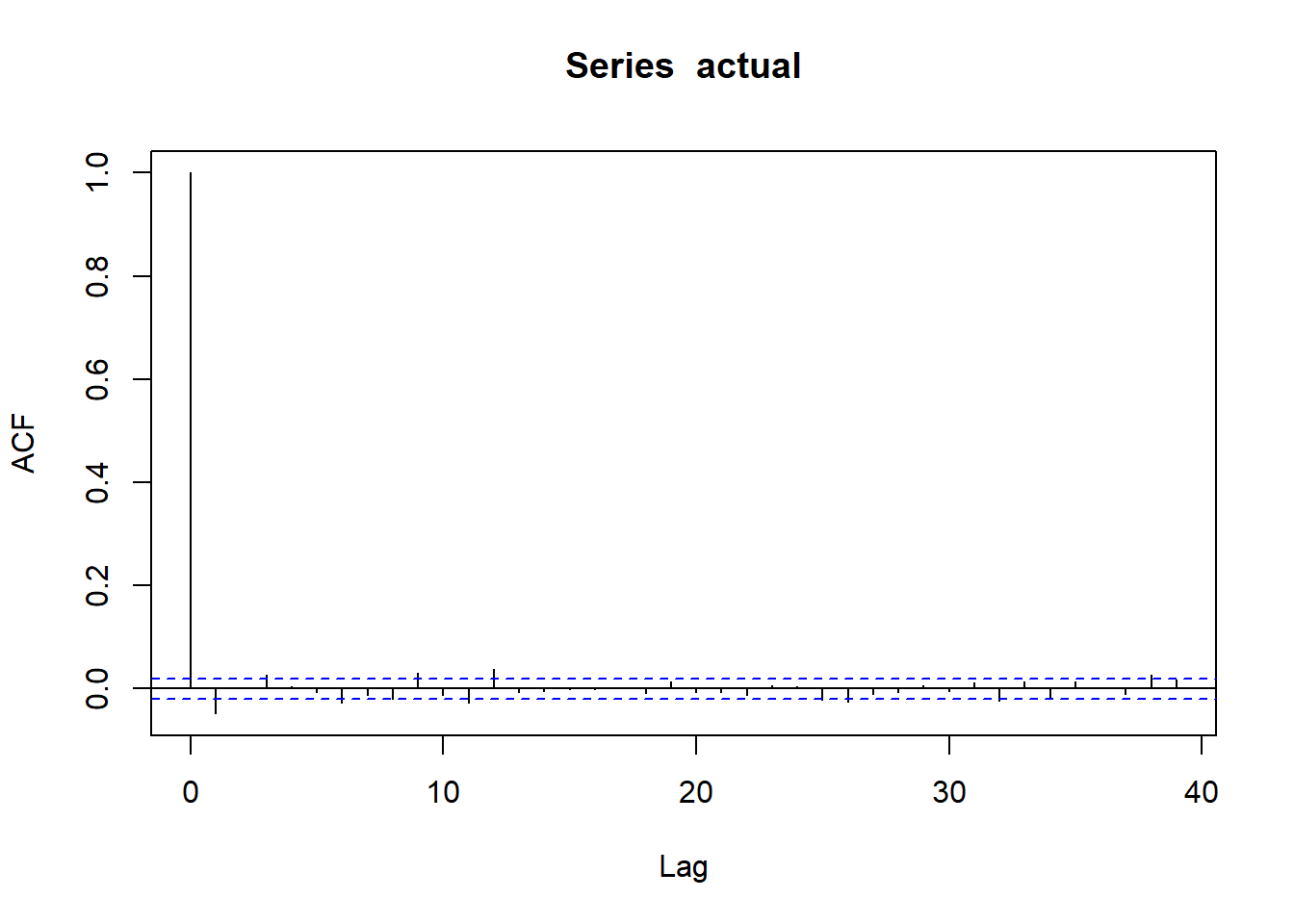

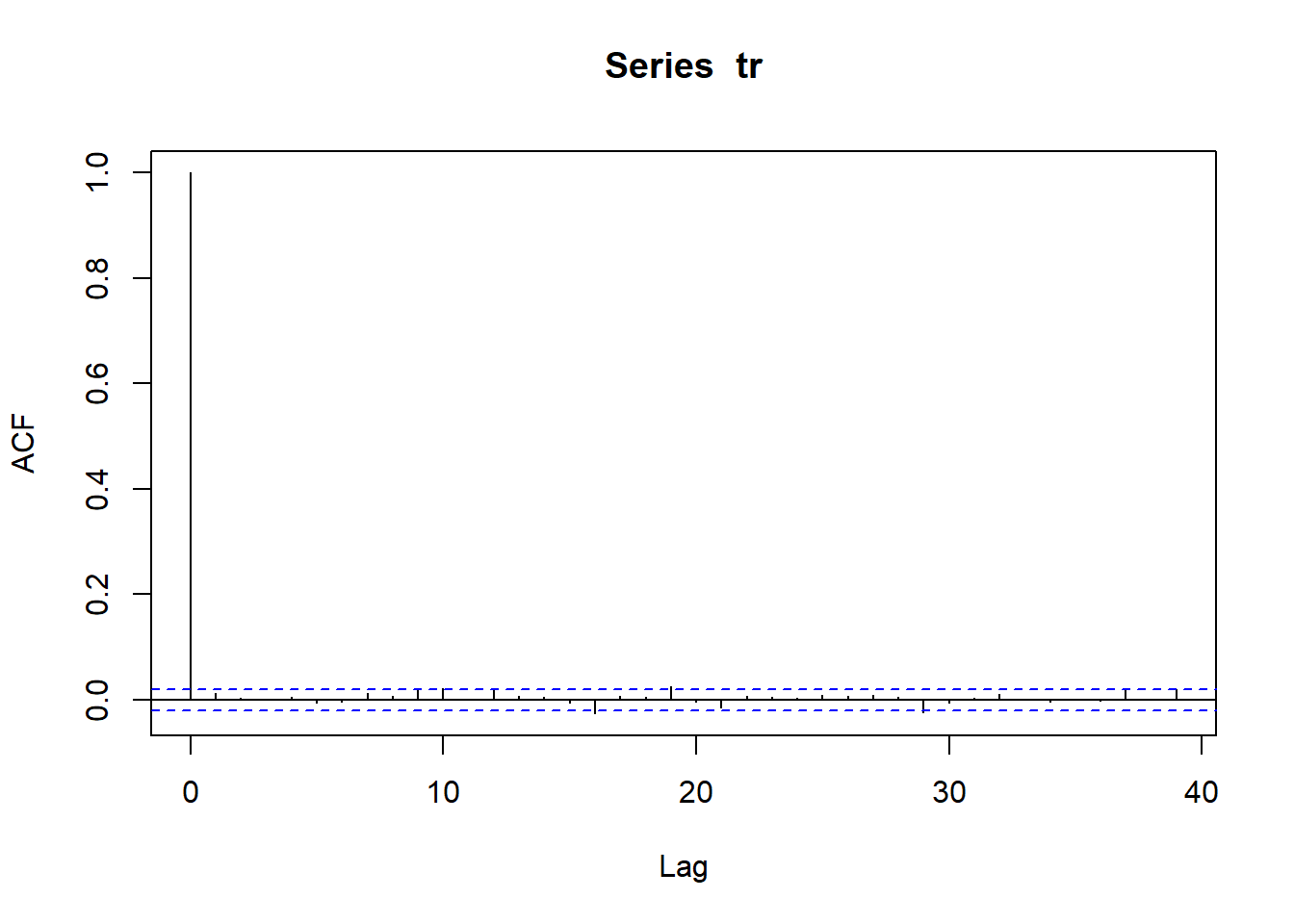

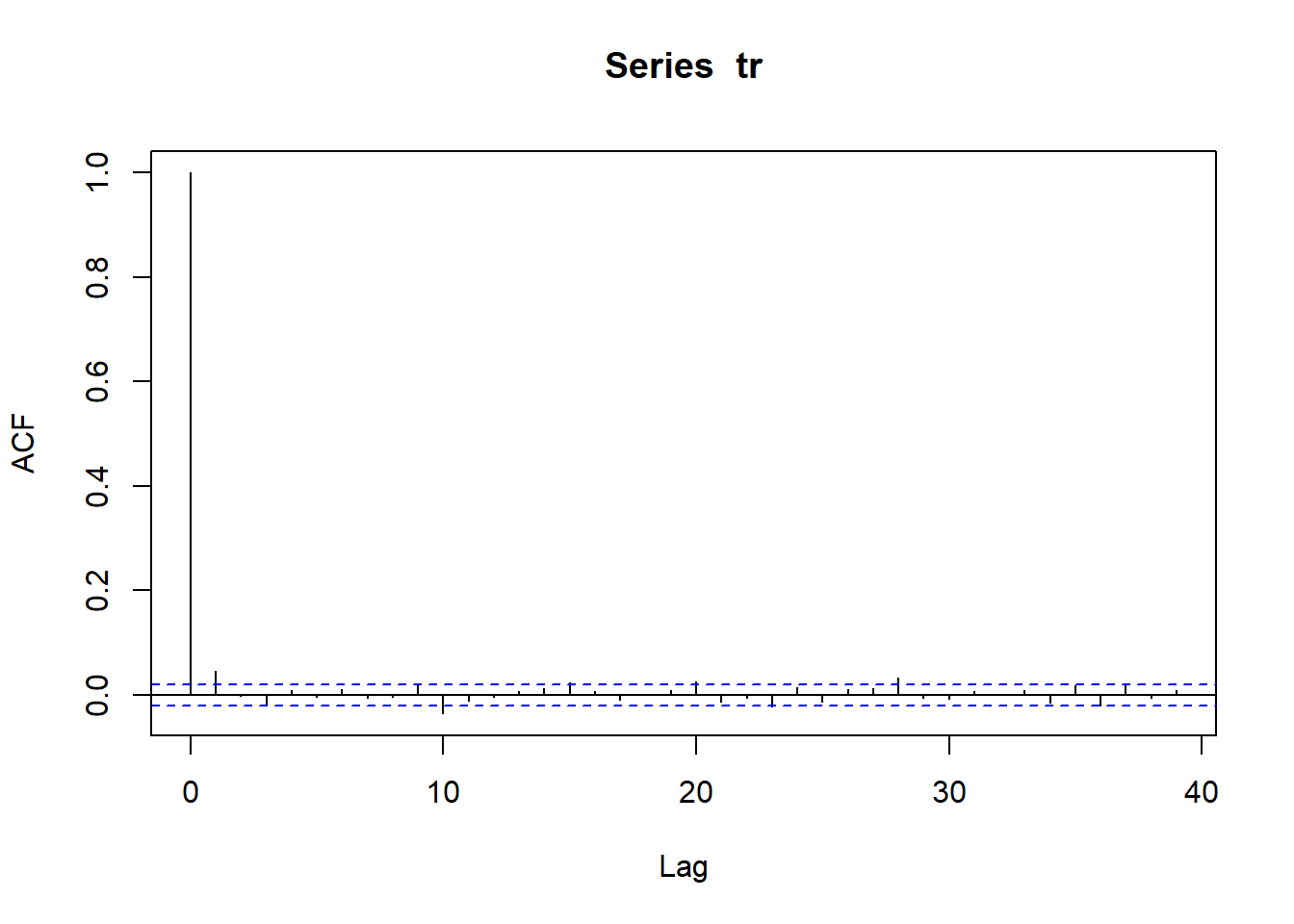

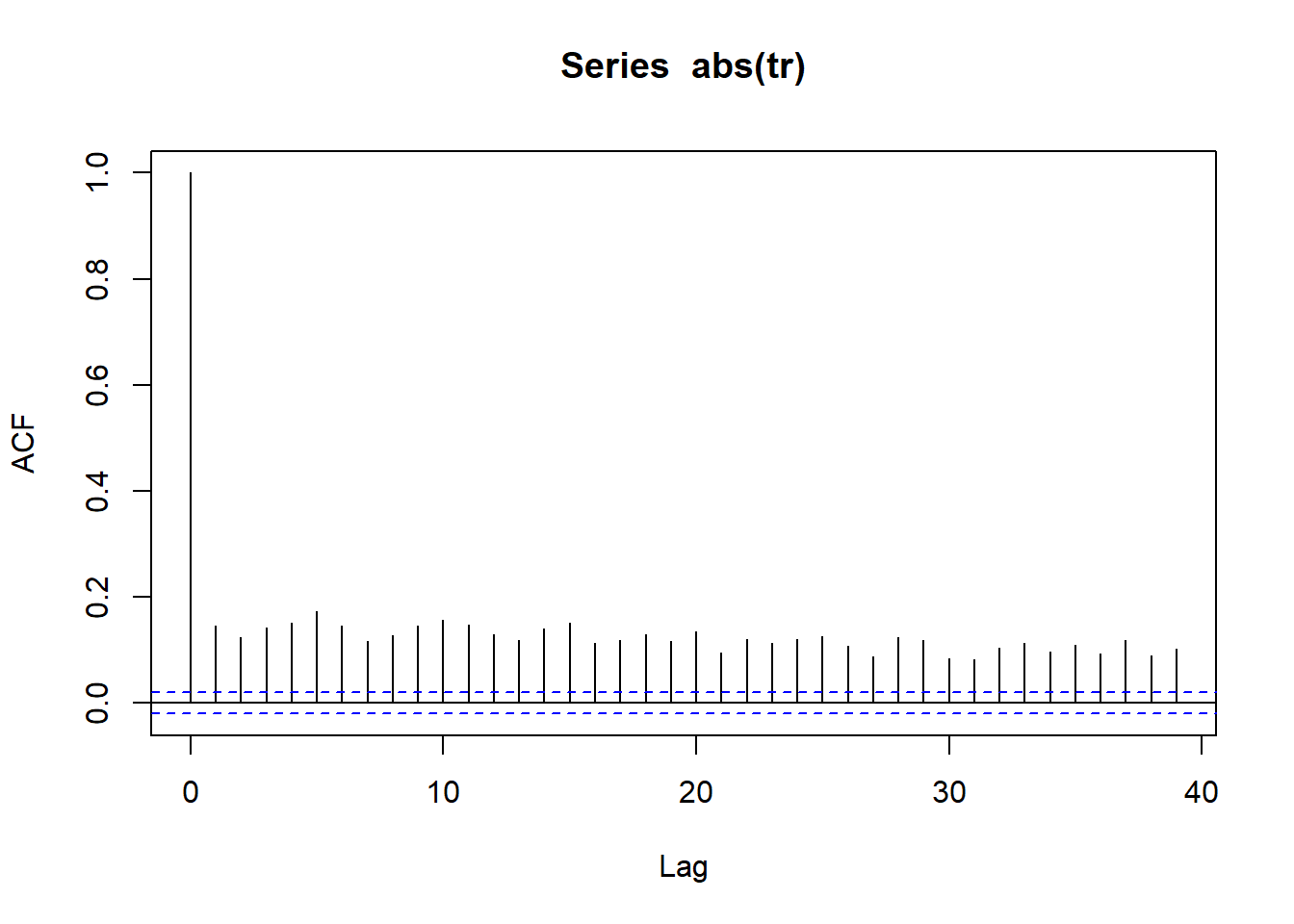

wilsh |>logret_1() |>acf()

ACF Intrepretation

Dashed lines represent 95% confidence interval for ACF

If many vertical lines are outside dashed band => We have evidence of serial correlation.

If all or most lines are inside dashed bands => no strong evidence of serial correlation.

Above plot shows , We do not find much evidence of serial correlation in the daily log returns of the Wilshire 5000 index. That means the direction of stock prices are not predictable.

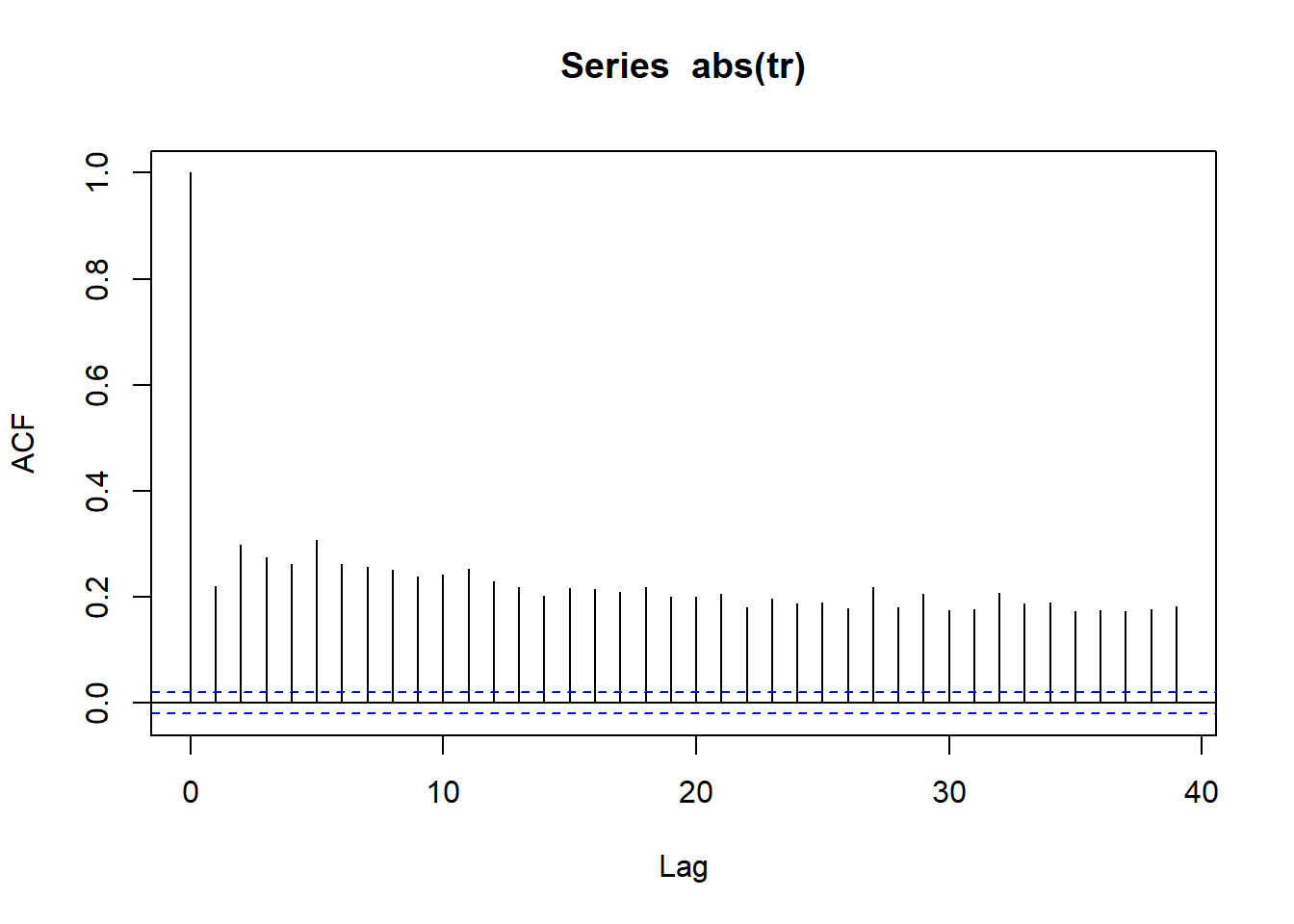

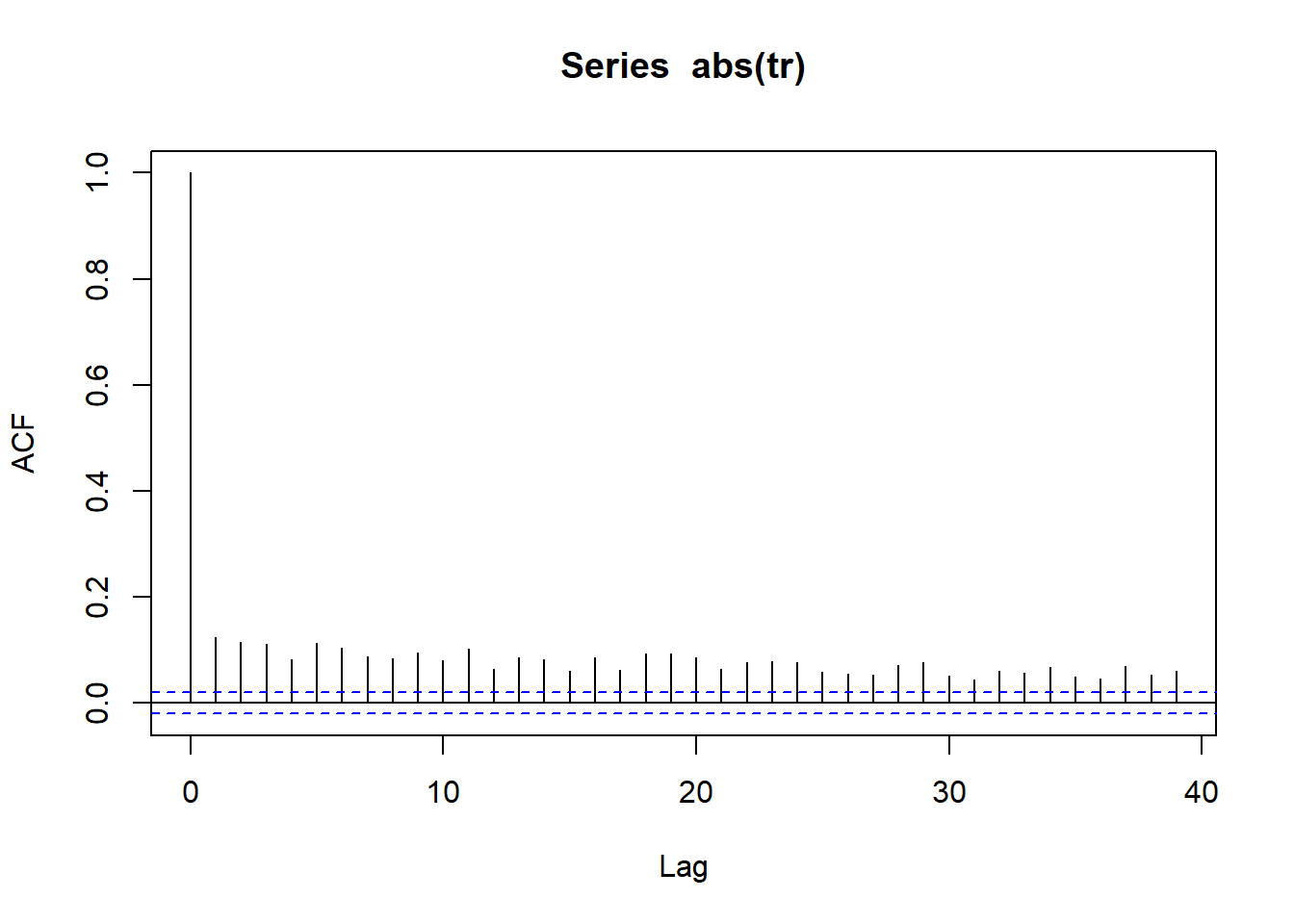

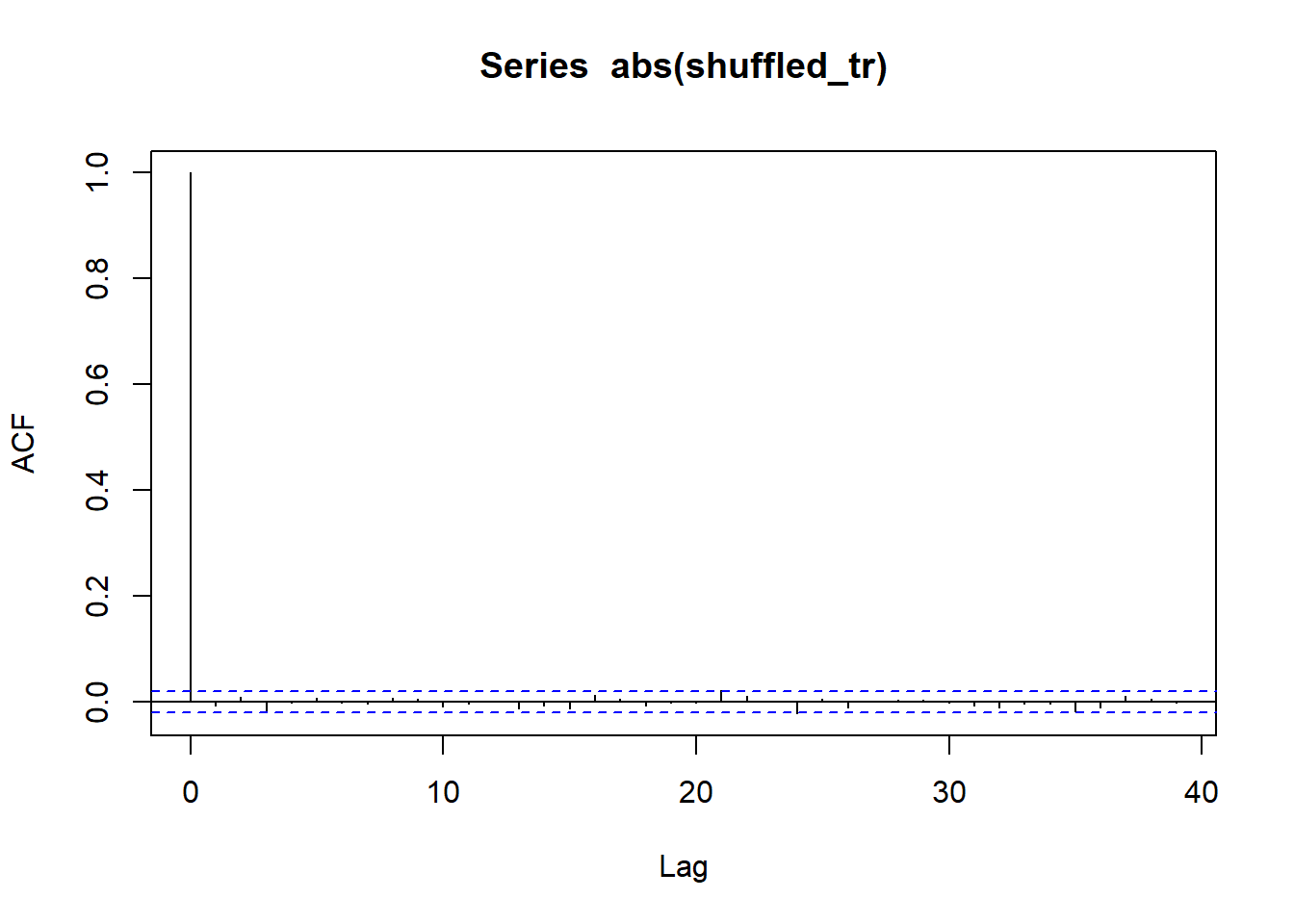

Volatility Clustering

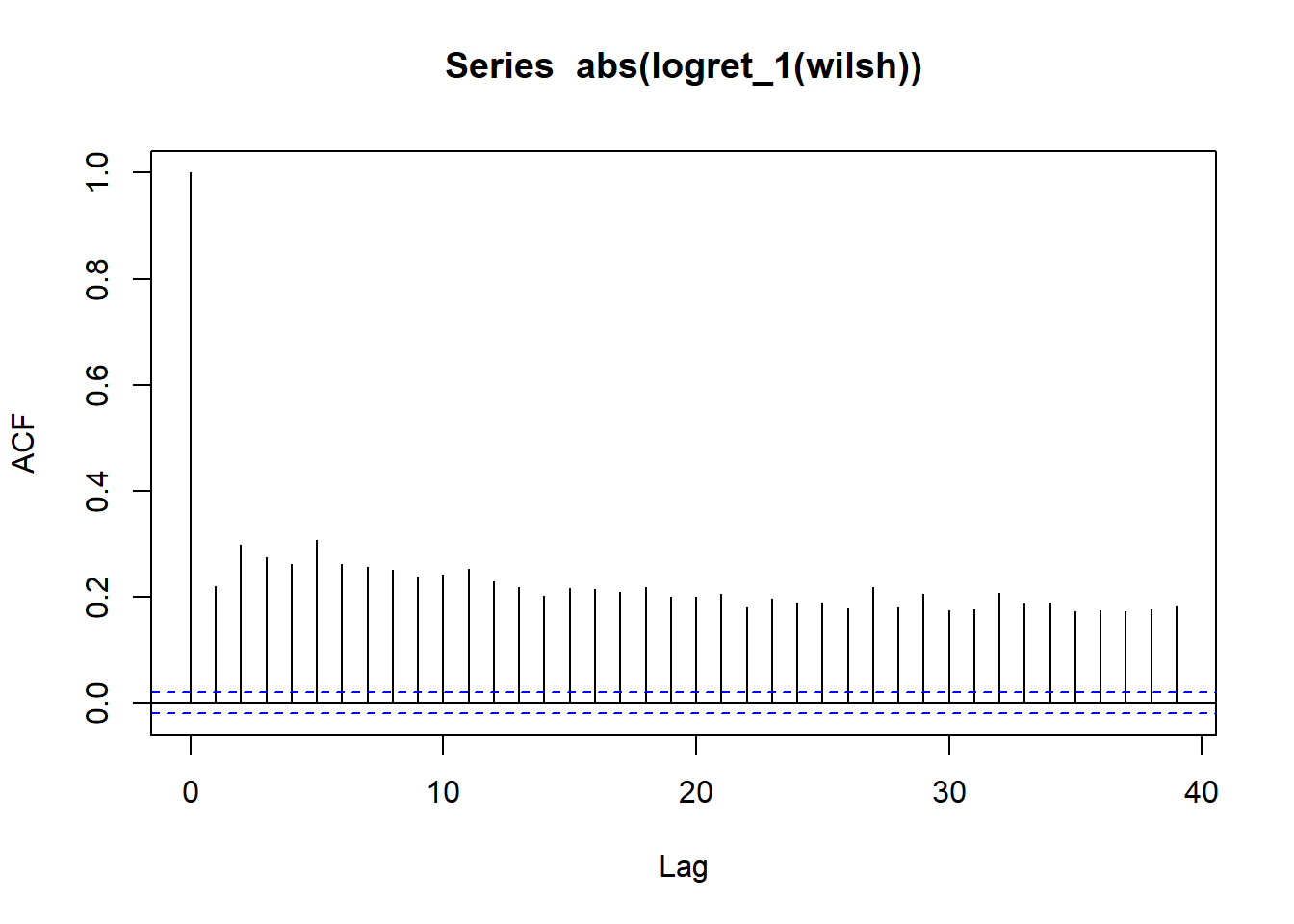

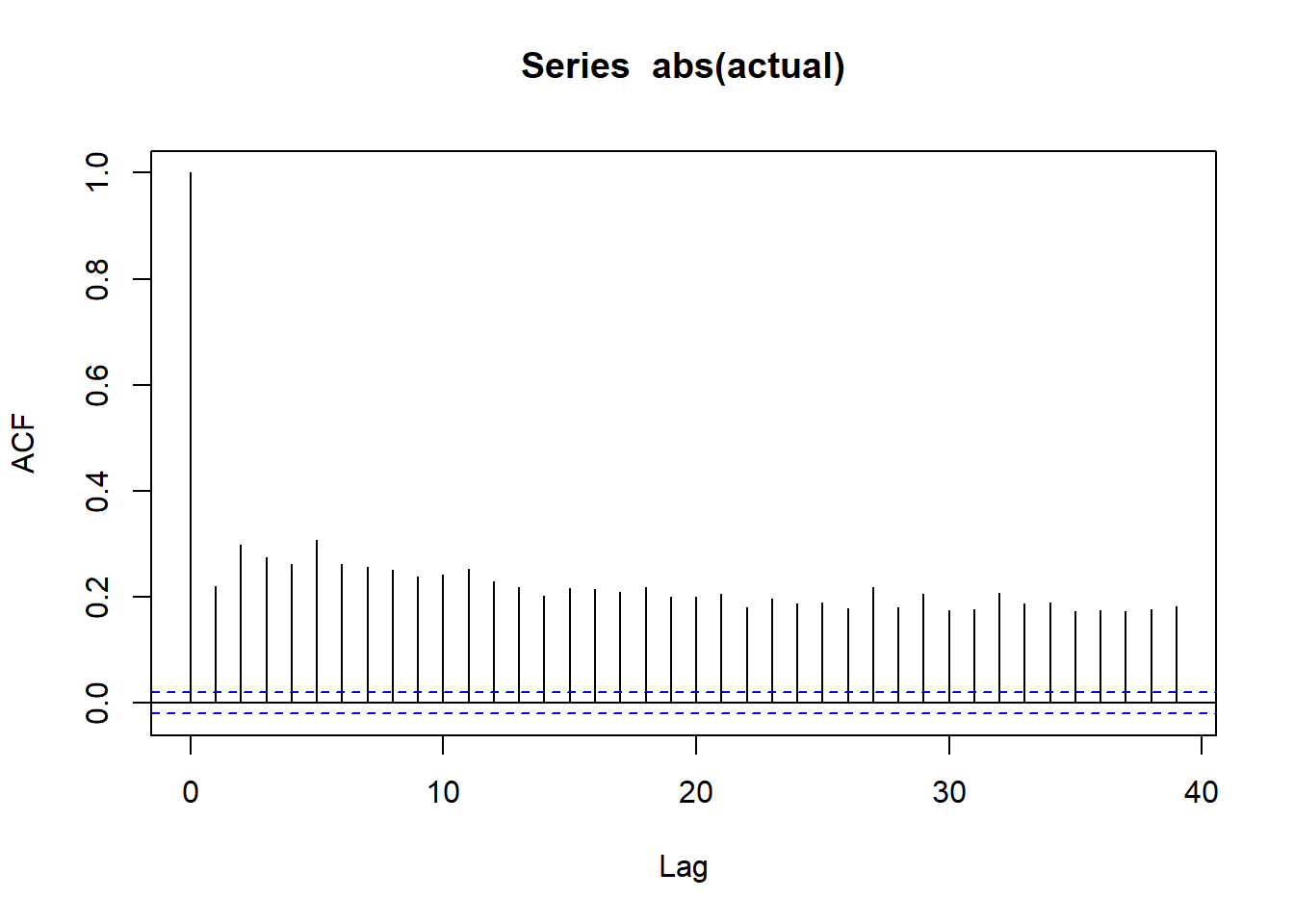

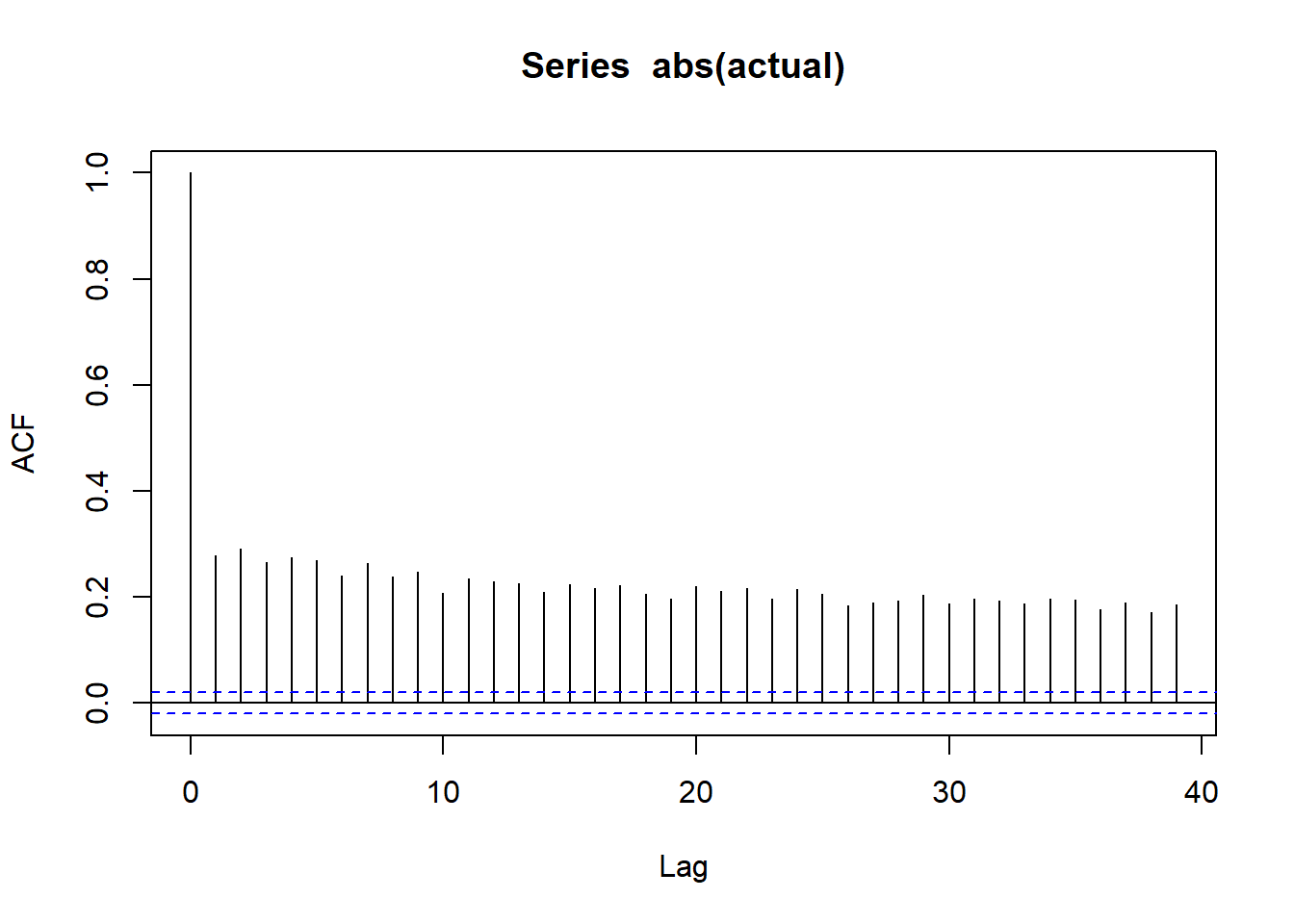

wilsh |>logret_1() |>abs() |>acf()

All lines for autocorrelation on absolute values are above dashed band showing strong possibility of serial correlation and thus volatility clustering

*---------------------------------*

* GARCH Model Spec *

*---------------------------------*

Conditional Variance Dynamics

------------------------------------

GARCH Model : sGARCH(1,1)

Variance Targeting : FALSE

Conditional Mean Dynamics

------------------------------------

Mean Model : ARFIMA(0,0,0)

Include Mean : TRUE

GARCH-in-Mean : FALSE

Conditional Distribution

------------------------------------

Distribution : norm

Includes Skew : FALSE

Includes Shape : FALSE

Includes Lambda : FALSE

g <- save1$zg |>as.vector() |>mean() |>round(digits=4)

[1] -0.0309

g |>as.vector() |>sd() |>round(digits=4)

[1] 1.0006

g |>as.vector() |>skewness() |>round(digits=2)

[1] -0.59

g |>as.vector() |>kurtosis() |>round(digits=2)

[1] 6.44

g |>as.vector() |>jarque.test()

Jarque-Bera Normality Test

data: as.vector(g)

JB = 5292.3, p-value < 2.2e-16

alternative hypothesis: greater

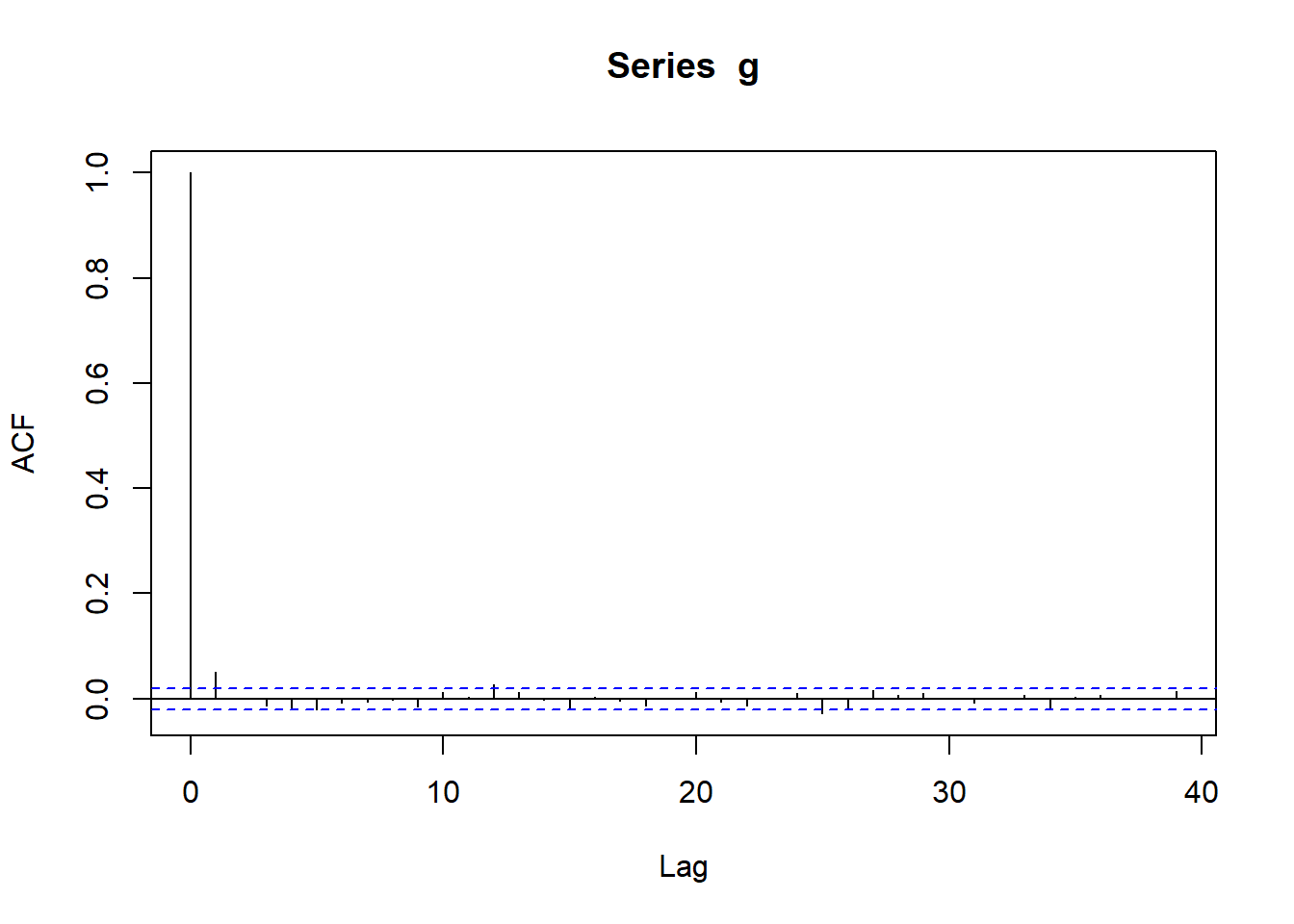

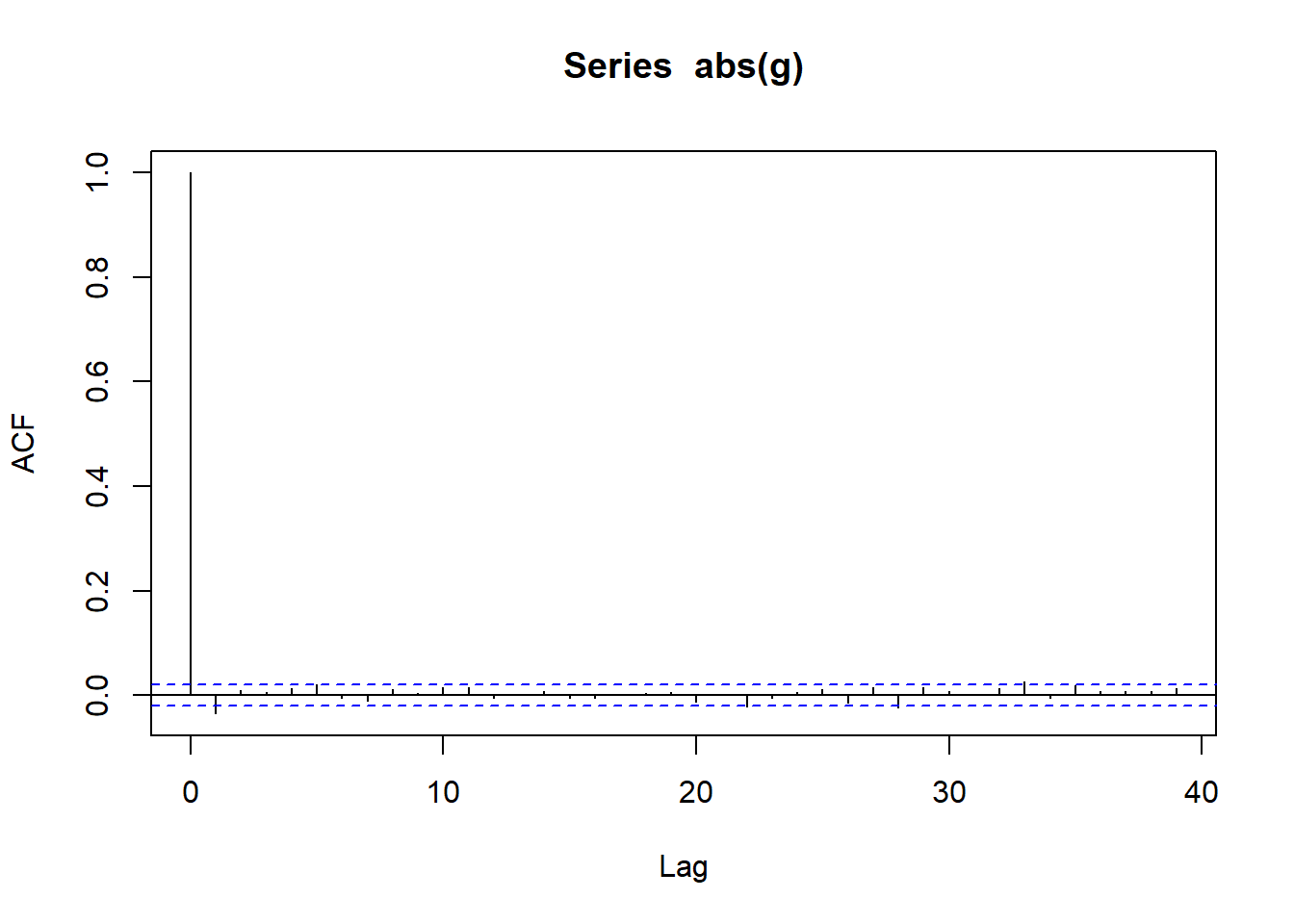

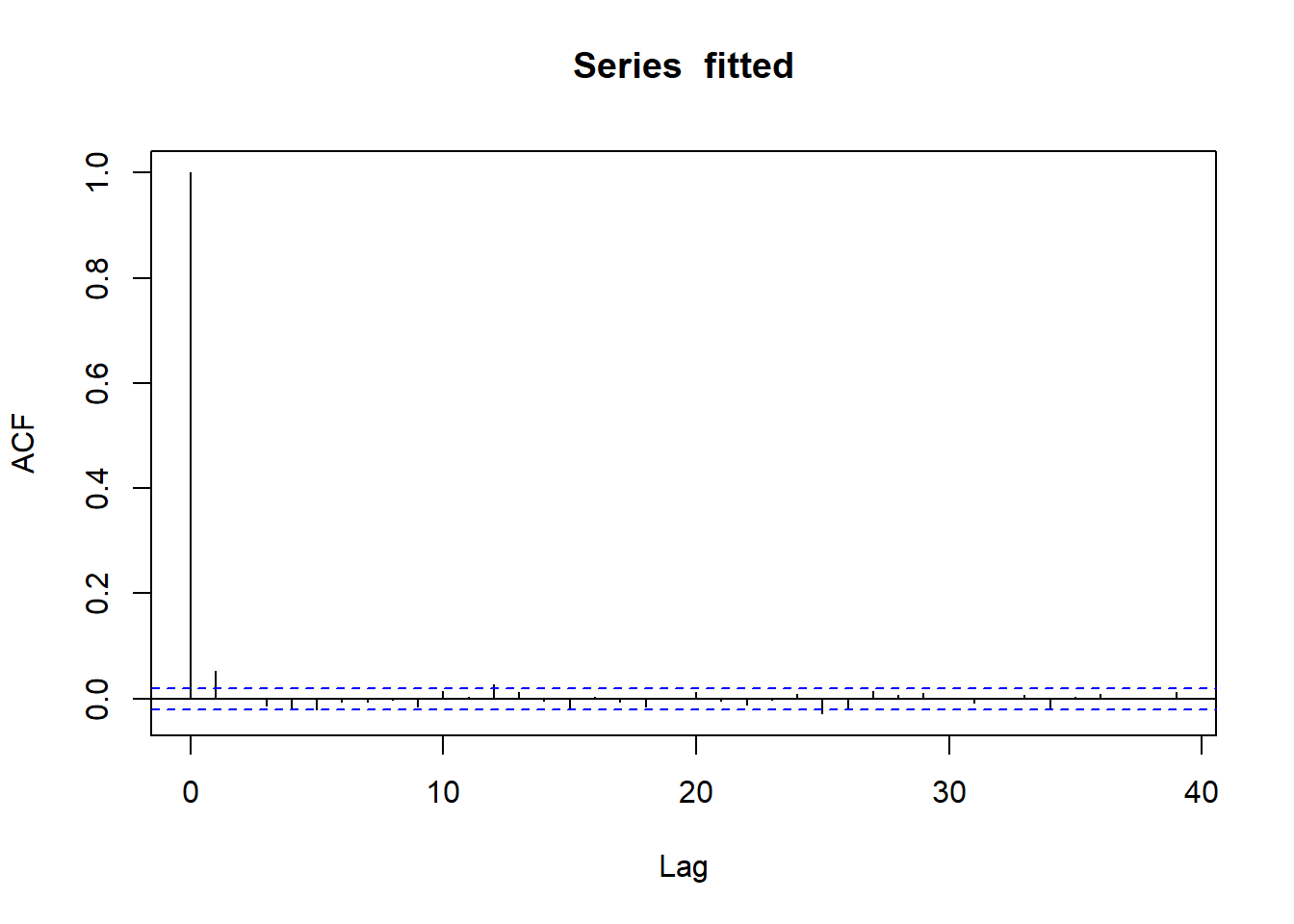

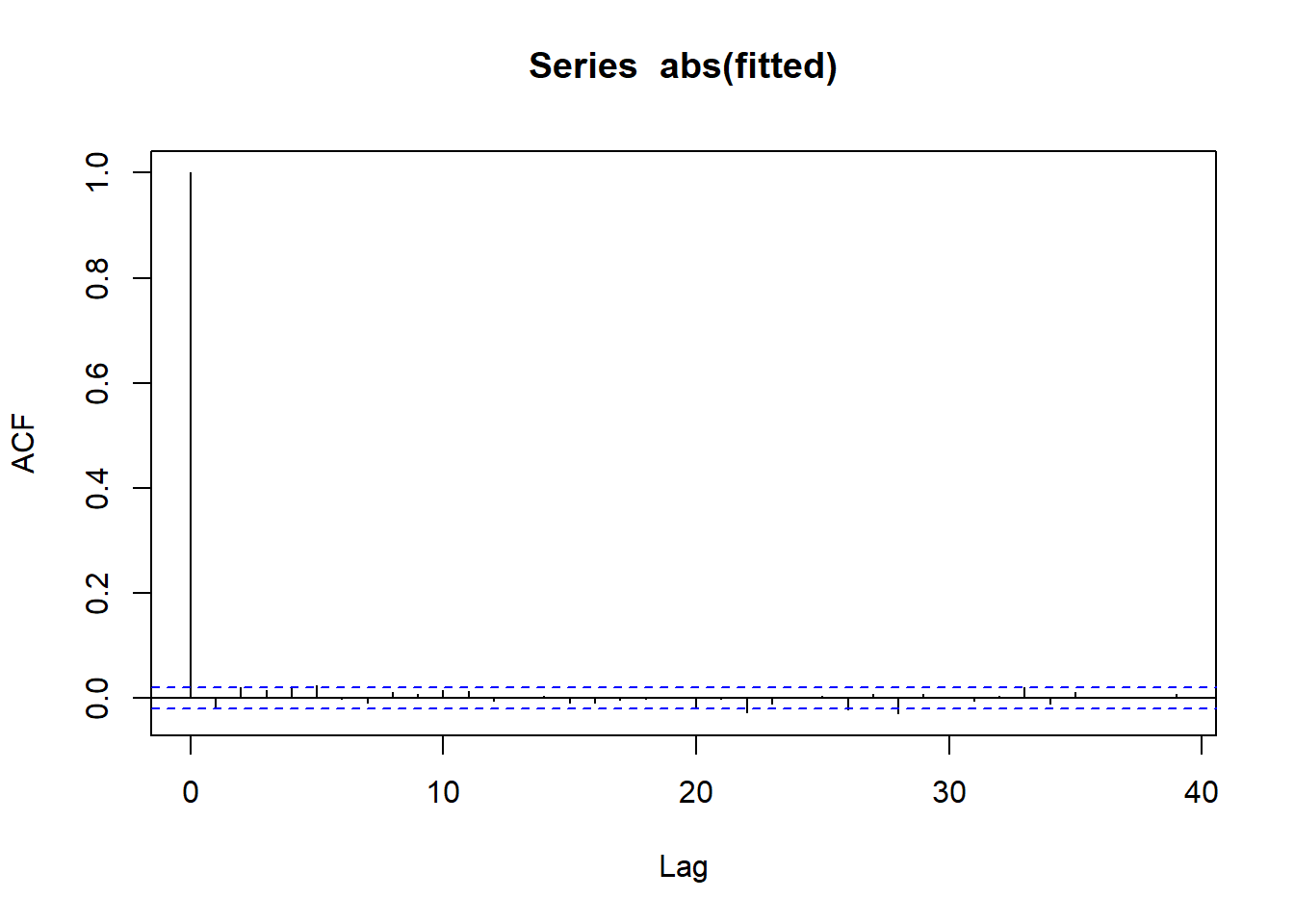

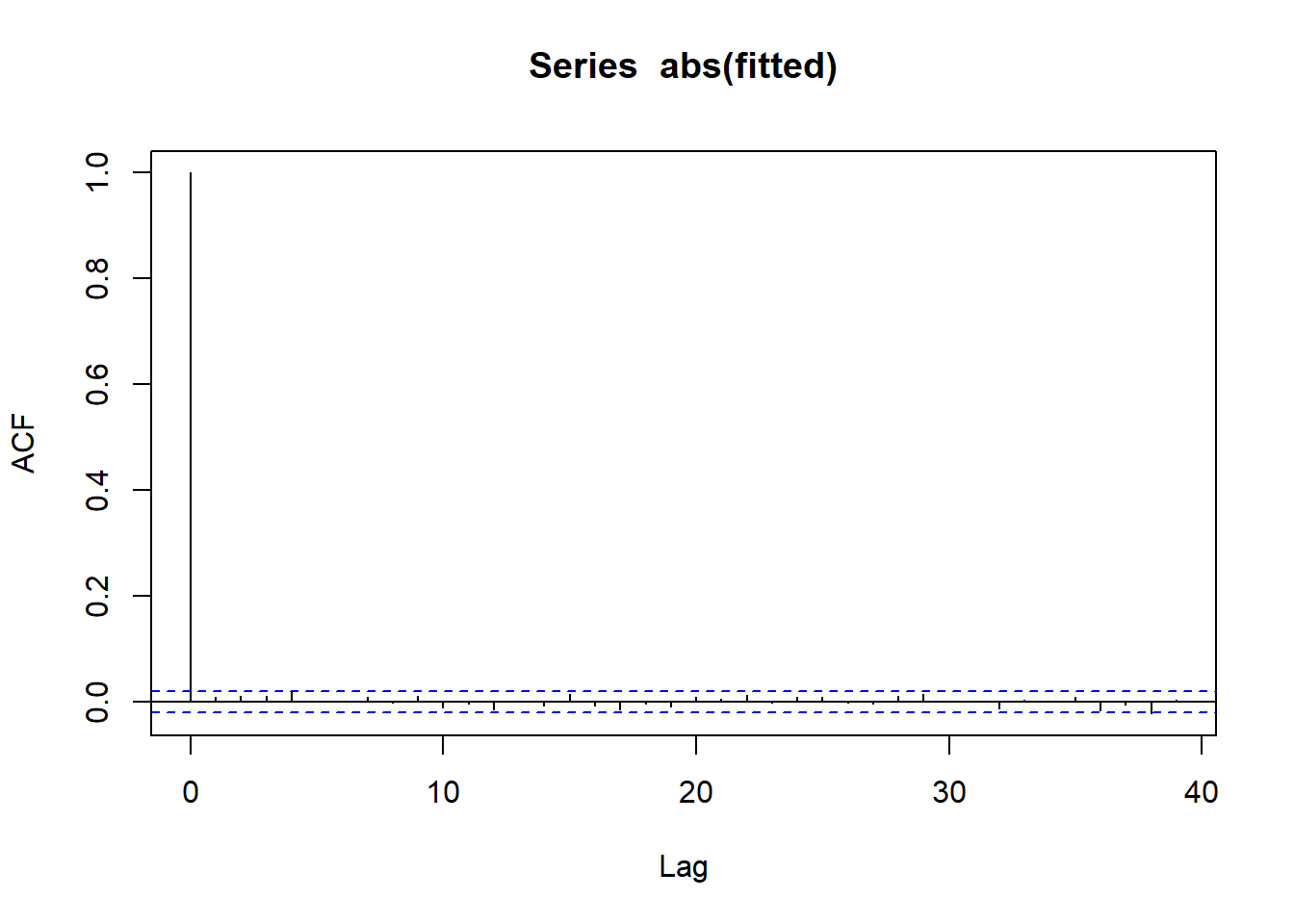

g |>acf()g |>abs() |>acf()

ACF of fitted e(t)

ACF of |fitted e(t)|

g <- save1$logretg |>as.vector() |>mean() |>round(digits=4)

[1] 4e-04

g |>as.vector() |>sd() |>round(digits=4)

[1] 0.0107

g |>as.vector() |>skewness() |>round(digits=2)

[1] -0.91

g |>as.vector() |>kurtosis() |>round(digits=2)

[1] 21.8

g |>as.vector() |>jarque.test()

Jarque-Bera Normality Test

data: as.vector(g)

JB = 142514, p-value < 2.2e-16

alternative hypothesis: greater

t <- g |>as.vector() |>jarque.test()t$statistic

JB

142514.5

t$p.value

[1] 0

t$alternative

[1] "greater"

Interpretation of Garch(1,1) - normal model

For a normal distribution to be true fitted e(t) should have

mean=0, sd=1, skewness=0, kurtosis=3

Jacque bera test should be able to confirm normality

Kurtosis of our data is around 21.8 . Our fitted distribution is around 6.44 and normal distribution expects it to be 3 => GARCH model is able to explain quite a lot but not all of the heavy tail

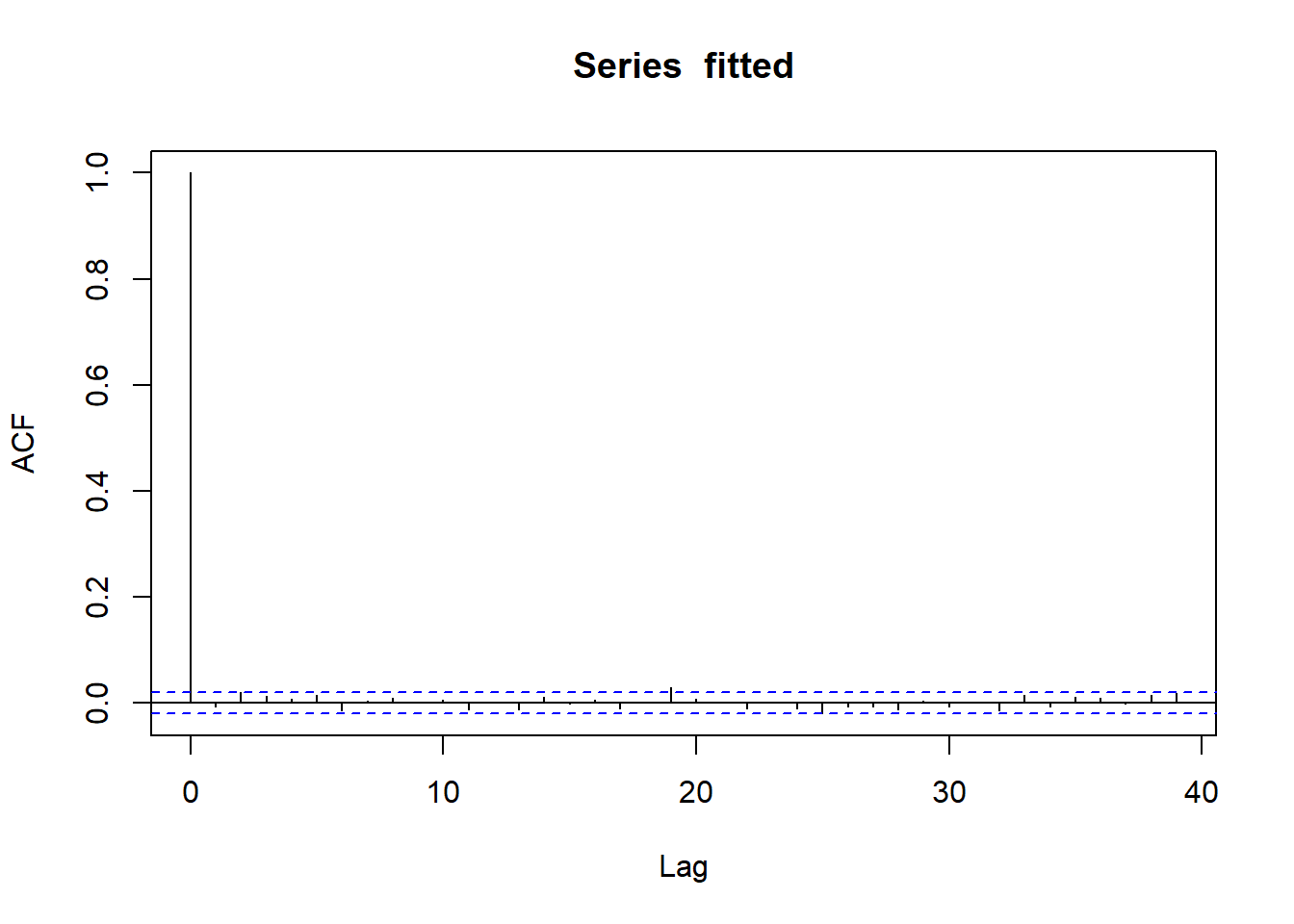

ACF curves for fitted value indicated no serial correlation

ACF curves for absolute fitted value indicate no serial correlation and thus, no volatility clustering => Variance equation in GARCH model is able to explain all volatility clustering in our data

Conclusion: GARCH(1,1) - normal model can explain

Volatility clustering of our data

Some but not all of heavy tails of the data

To have better explanation of distribution we need to change distribution equation.

g <- gold |>filterSeries() |>logret_1()g |>head(2)

TR

1980-01-03 0.12500543

1980-01-04 -0.07532201

g |>tail(2)

TR

2017-12-27 0.011674890

2017-12-28 0.009025894

g |>do_analysis_garch_nextday(date.ends=c("2017-12-29","2008-09-15","1987-10-19")) |>format(digits=5)

Warning in RNGkind(sample.kind = "Rounding"): non-uniform 'Rounding' sampler

used

Warning in RNGkind(sample.kind = "Rounding"): non-uniform 'Rounding' sampler

used

Warning in RNGkind(sample.kind = "Rounding"): non-uniform 'Rounding' sampler

used

g |>get_garch_VaR_plot(refit.every =100, alpha =0.05)

Warning in RNGkind(sample.kind = "Rounding"): non-uniform 'Rounding' sampler

used

Warning in RNGkind(sample.kind = "Rounding"): non-uniform 'Rounding' sampler

used

Warning in RNGkind(sample.kind = "Rounding"): non-uniform 'Rounding' sampler

used