In real life many distribution are non-normal => We find skewness in distribution of data.

Distribution of how many cups of coffee some one drinks a day/ alcohol

Non drinkers - Data Clustered at zero

Low/Moderate drinkers range of usage

Addicts/ Alcoholics -Heavy drinkers

Ways data ( here financial data ) can depart from normality

Skewness - right tail left tail [ left skewed if left tail is longer than right tail]

Kurtosis - Heaviness of tails of distribution

Other ways also exists

High freq data - daily log returns are typically not normal

VaR and ES depends on left tail of returns distribution(data) so their value is impacted by nature of distribution.

What happens when the data / left tails of return is skewed but we assume it’s normal and therefor symmetric.?

If distribution is left skewed it has a much longer left tail than symmetric or longer distribution => Large negative returns are more likely in left skewed graph than the middle graph => More negative VaR and ES values.

What is the implication of heavy tailed distribution on VaR and ES?

Large outcomes positive / negative more likely in heavy tailed distribution than normal distribution => VaR and ES will not be correct when assuming normal distribution.

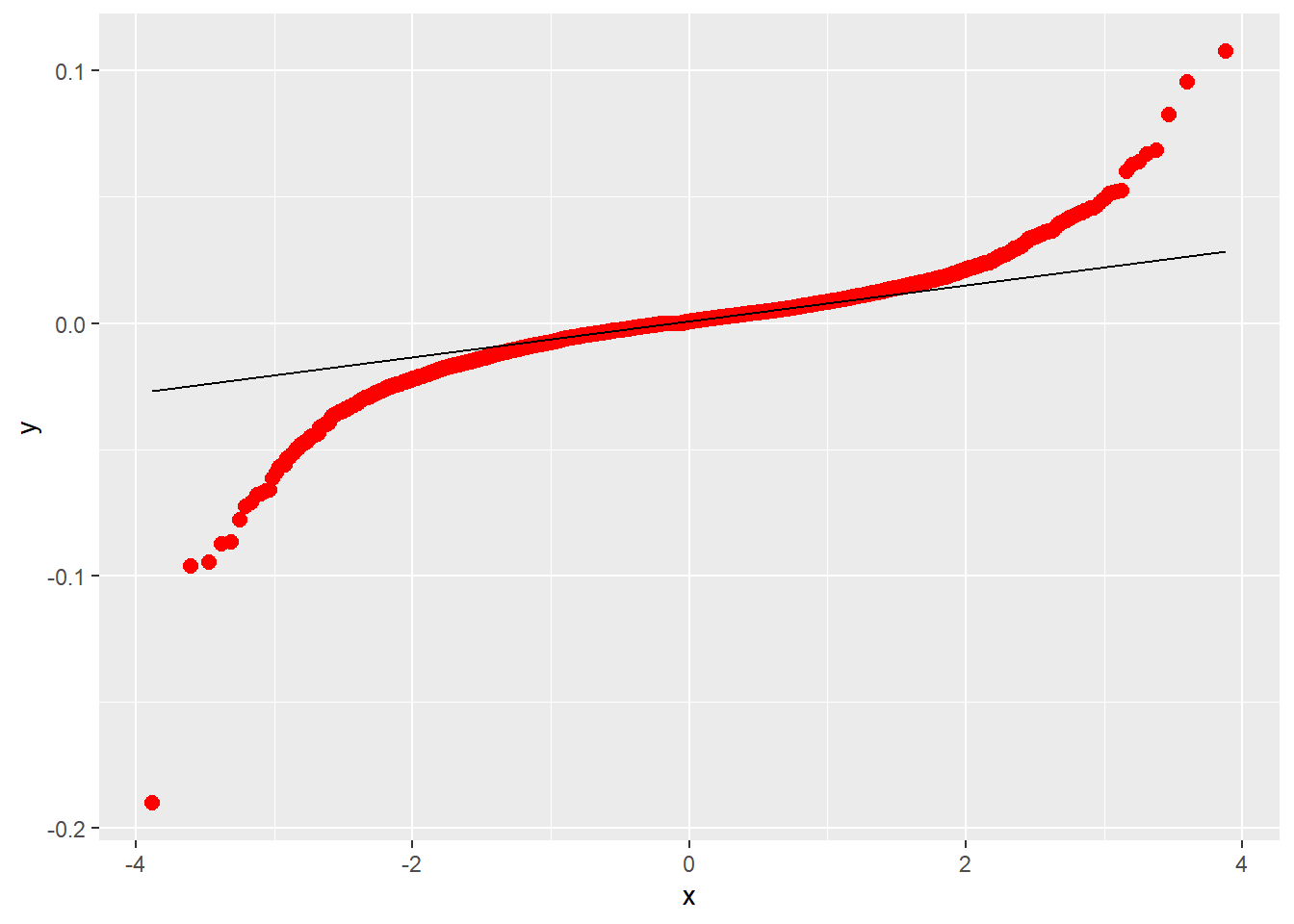

Test for normality

Jarque Bera Test ( JB Static very large with p-value zero -> reject normality

QQPlot

Kolmogorov-Smirnov Test: Histogram of actual data against histogram of assumed normal distribution

If data is not normal

Find a distribution which describes our data better than the normal distribution

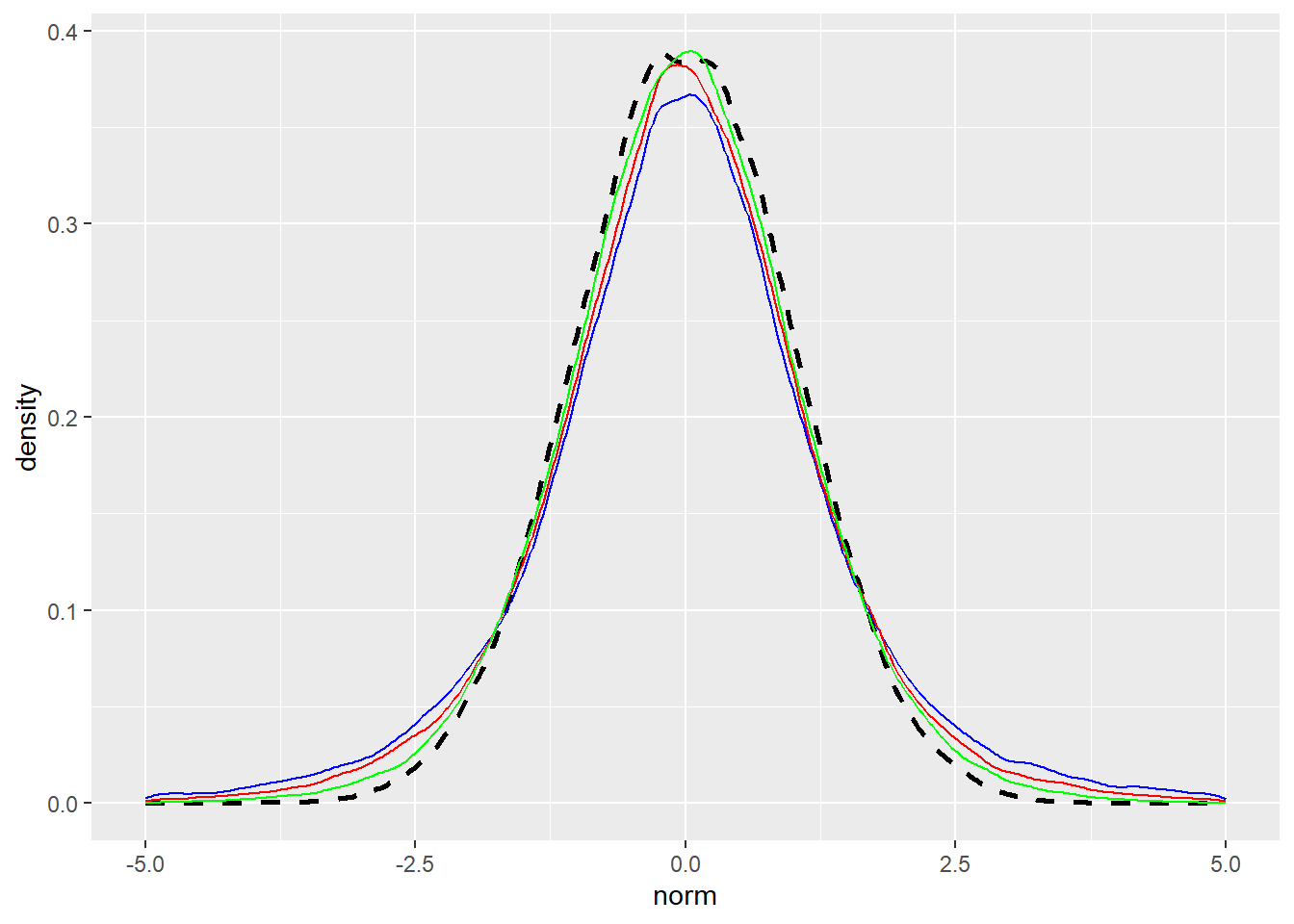

In this week we use Student-T Distribution.

Student T Distribution

Described by mean . sigma and degree of freedom(v)

Mean always 0

Variance

Skewness 0 for v> 3 otherwise undefined

Kurtosis 3+ 6/(v-4) for v>4, infinity for 2 < v <= 4, otherwise undefined

At v -> infinity , it is normal distribution.

Implies, T-distribution family include normal distribution as a special case.

Degree of freedom controls the shape of the distribution

Student T- has heavier tail than normal (Kurtosis=3)

Differ from normal distribution in term of

Same mean and Skewness

Differ Std. Dev - not that important

Kurtosis is higher

Degree of freedom get larger =>Kurtosis get’s smaller.

How do you match Student-T distribution to data?

Problem - Find distribution which match standard deviation and Kurtosis student T distribution to the data.

Since we only have single parameter here which is v. We do a trick to solve

We need to create 2 equation with 2 unknown => Use Rescaled T-distribution.

Divide distribution by root of v/v-2.

First find v by matching kurtosis value of data with Rescaled T-Distribution.

Pick a scaling parameter to match standard deviation of data.

s <- wilsh |>logret_1() |>logret_ndays(days=10) |>get_sim_series()VaR <- s |>get_sim_VaR(alpha=0.05); VaR

[1] -0.04700005

ES <- s |>get_sim_ES(VaR=VaR); ES

[1] -0.07780043

This is probably a nicer way to simulate block based simulation first by calculating logret_10 and then simulating the regular series. Only challenge is because of randomness, we can’t match results with exactly with random number seed process. So let’s implement a block based approach that exactly matches our answer from presentation.